China's GDP Target Hits 35-Year Low: Has Beijing Finally Stopped Pretending?

China's 2026 GDP target drops to 4.5%-5%, the first time below 5% in 35 years. Rhodium Group estimates real growth at just 2.5%. Wen Jiabao's warning from 13 years ago is coming true.

China announced its 2026 GDP growth target today: 4.5% to 5%.

The world's second-largest economy can't even commit to a whole number. In the 2022 work report, they wrote "around 5.5%" in black and white, then delivered 3.0% for the year — a globally broadcast slap in the face. Since then, Beijing learned a lesson: the vaguer the target, the less obvious the swelling. Xinhua calls this "policy flexibility." Normal people call it leaving yourself an escape route.

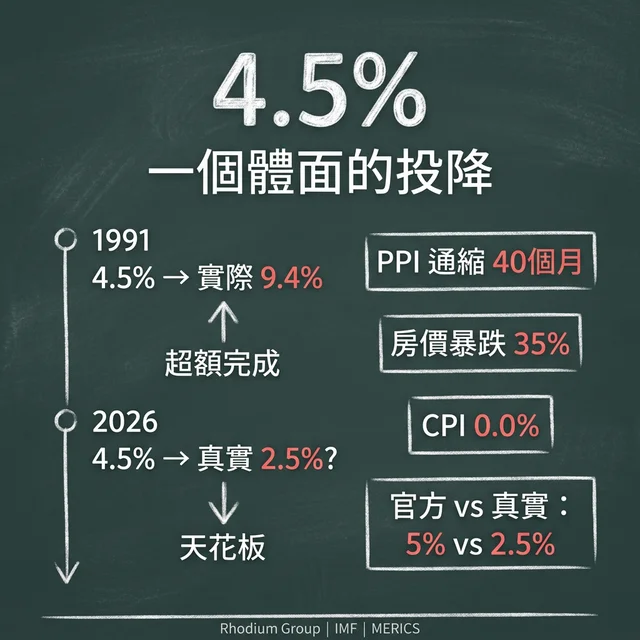

The last time the GDP target was below 5% was 1991. That year they set "around 4.5%" and actual growth came in at 9.4%. The Great Hall of the People erupted in applause. "Exceeding the target" is the Chinese Communist Party's favorite four-character phrase. Thirty-five years later, the same number returns, but the applause is gone — this time, 4.5% isn't false modesty. It's the ceiling they're hitting with everything they've got.

Li Qiang stood at the podium reading from his script, and every economist in the world had the same question: Is this number real?

The Officialese Translation Machine

Yu Miaojie, president of Liaoning University, said the range target "grants greater policy flexibility, allowing local governments to focus more on people's livelihoods." That same day, in the same government work report, the budget for consumer trade-in subsidies was slashed from 300 billion to 250 billion yuan. Championing livelihoods on one hand, gutting the only program actually spending money to stimulate consumption by 50 billion on the other. All ideology on the lips, all business in the heart.

NDRC Vice Chairman Wang Changlin publicly admitted China's economy suffers from "strong supply, weak demand." In plain English: factories are churning out products like mad while nobody's buying. PPI deflation has exceeded 40 months — possibly the longest streak since records began. Full-year CPI came in at 0.0% — against a target of 2%, they turned in a precise zero. December 2025 retail sales grew 0.9% year-over-year, the lowest since the end of lockdowns in late 2022. Consumer confidence index: 89.50, against a historical average of 108.68 and a peak of 127. Which part of "stable and improving" is the "improving"?

Ordinary people aren't spending because they're terrified. Home prices have plunged 35% from their 2021 peak. New home sales collapsed from 18.2 trillion to 8.4 trillion yuan — calling it "halved" is being generous. Seventy percent of household wealth is locked up in bricks, and the bricks are melting. S&P says prices could fall another 10% to 14%. Seventy-seven developers have defaulted. Evergrande, with $360 billion in liabilities, has been liquidated and delisted. Country Garden, with $200 billion in debt, just completed its offshore restructuring. National housing inventory has ballooned to 27 months, with third and fourth-tier cities at 40 months. S&P's description: structurally entrenched. This isn't waiting for a bottom to bounce — the terrain itself has deformed.

Goldman Sachs chief China economist Hui Shan says if China follows the typical timeline of global real estate collapses, home prices could still have 10% of downside, with nationwide real prices not bottoming until 2027. And she's the loudest voice among the optimists.

An Insider's Indictment

Foreign criticism can always be dismissed as "hostile foreign forces smearing China" by the Global Times. When your own people speak up, there's nowhere to hide.

Former PBOC advisor Liu Shijin said: "China's current consumption shortfall is deeply intertwined with a series of institutional and structural factors. Fully resolving this in the short term is unrealistic, but leaving it unaddressed is not an option either."

In 2012, Wen Jiabao said at the NPC press conference: "Without the success of political system reform, economic reform cannot be carried through to the end, and gains already achieved could be lost." Thirteen years later, political reform never happened, and the economic gains are being lost.

Institutional, structural, deeply intertwined — both Wen Jiabao and Liu Shijin point in the same direction: this isn't a cyclical downturn. It's a systemic illness. Daron Acemoglu won the Nobel Prize for proving exactly this — institutions determine destiny. The CCP's system doesn't have the flu and need medicine. Its DNA is defective.

The Mercator Institute for China Studies (MERICS) puts it even more bluntly. Beijing talks about stimulating consumption, but what it truly believes is something else entirely: in an era of great power competition, pouring money into chip manufacturing and EV subsidies is more "worthwhile" than letting ordinary people — sorry, "the masses" — have money to spend. So-called "high-quality development" isn't tailored for the people. It's a bespoke suit for industrial policy.

Whose 5% Is It?

Can official GDP numbers be trusted?

Rhodium Group estimates China's real 2025 growth at 2.5% to 3.0%. The official figure: 5.0%. Nearly double the gap. Rhodium flags a problem the National Bureau of Statistics still refuses to address: fixed asset investment fell 3.8% in 2025, yet the investment component in the GDP report shows a positive contribution. The arithmetic doesn't add up — any schoolchild can see it. Unless you treat GDP as a political product rather than a statistical one — then everything makes perfect sense.

The 2026 forecast is worse: real growth of 1% to 2.5%. Rhodium's exact words: "History does not provide examples of economies achieving 5% real GDP growth while enduring deflation as China has for consecutive quarters. We are skeptical that China will be the exception." Simply put: keep making things up.

IMF Managing Director Kristalina Georgieva urged Beijing to make "the brave choice" and accelerate structural reform. In diplomatic circles, using the word "brave" means what you're currently doing is anything but brave. Range targets that blur expectations, industrial subsidies replacing consumption stimulus, gradualism buying time — none of this is reform. It's painkillers. The pain comes back when they wear off.

Starting Line and Ceiling

Thirty-five years ago, the 4.5% was theater. Beijing knew full well the economic engine was accelerating. They deliberately lowered the target, waiting to "exceed" it at year's end — standing ovation, visionary leadership. That 4.5% was a booming economy pretending to be modest.

Thirty-five years later, the 4.5% is a decelerating economy's last shred of dignity.

Xi Jinping's goal of doubling per capita GDP by 2035 requires average annual growth of 4.17%. If Rhodium's estimates are even directionally correct, real growth over the past few years has already drifted far from that line — the NBS numbers have been maintaining a thin layer of reassurance for everyone. But reassurance has an expiration date. When the cost of fabrication exceeds the price of truth, even a range can't contain it anymore.

Same number, same Great Hall of the People, same regime. Thirty-five years ago, no range was needed — they were sure they'd win. Today a range is needed — because even they aren't sure how much longer they can keep winning.

Putting on a brave face. Only this time, the face is so swollen that even a range can't hide it.

_(Data sources: Chinese Government Work Report, National Bureau of Statistics, Rhodium Group, S&P, Goldman Sachs, IMF, MERICS, ING, Trading Economics, Macquarie.)_

_—Kinney's Wonderland_