When the Cannons Roar, Gold Crashes: The 'Safest' Asset Lost More Than Stocks in One Week

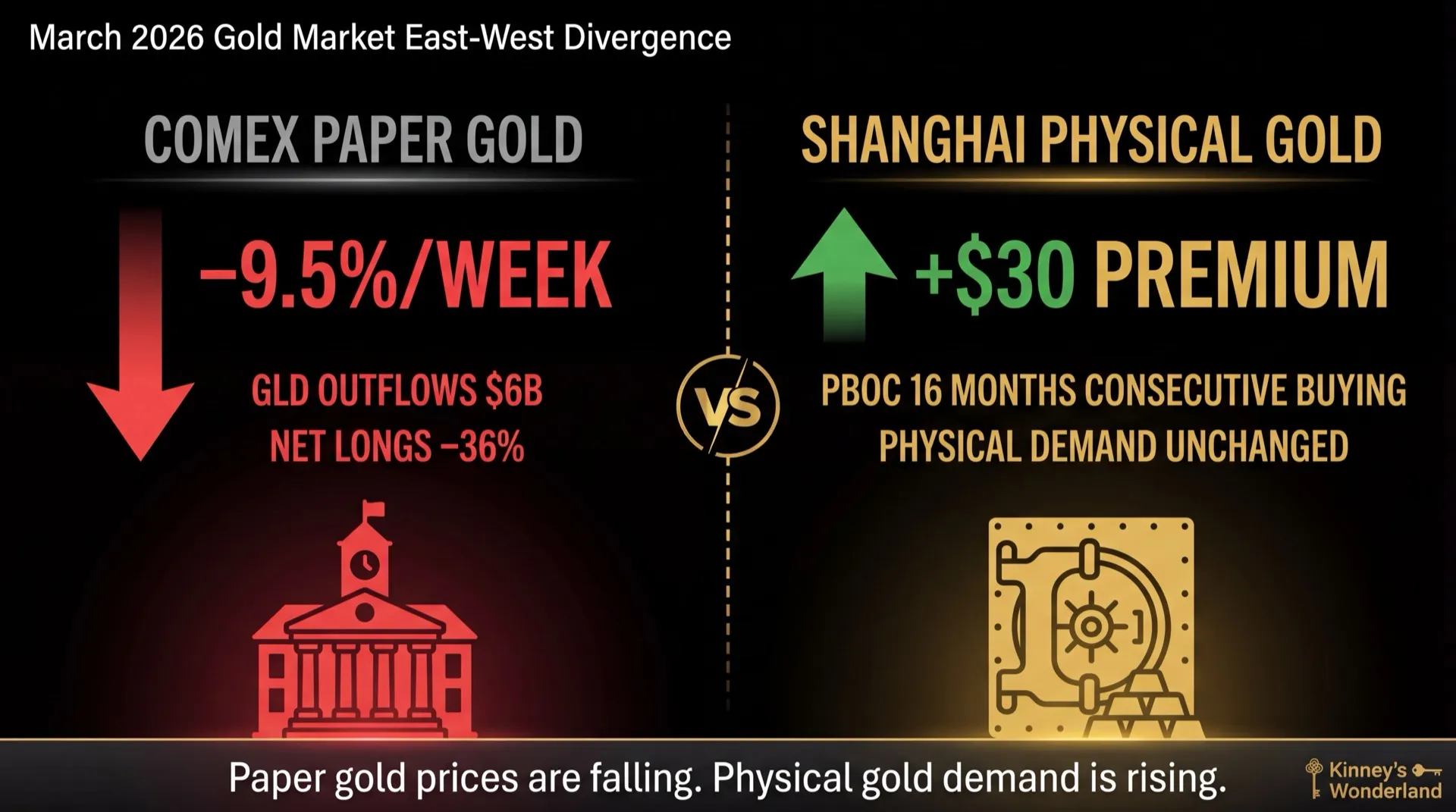

The Iran War was the biggest geopolitical crisis since 2003. Gold crashed 9.5% in one week. Because gold insurance only pays out when the Fed can cut rates. When war drives inflation, the Fed's hands are tied, and gold loses its engine. Yet Shanghai's physical gold premium hit +$30. Paper gold crashed. Physical demand didn't.

"When the cannons roar, gold soars."

Investors worldwide have treated this axiom as gospel, right alongside "buy and hold" and "don't fight the Fed," three of the safest clichés in finance. The logic sounds bulletproof: the more chaotic the world gets, the more people need a hard asset beyond any government's control. Gold, humanity's monetary anchor for millennia, is the ultimate insurance policy.

On March 20, 2026, the world finally got its perfect test case. The Iran War entered its third week. Four Gulf states had been hit simultaneously by Iranian missiles. The Strait of Hormuz was effectively blockaded. Brent crude had surged 57% in one month to $112.50 per barrel. The Fear & Greed Index hit 15, "Extreme Fear." This was the biggest geopolitical crisis since the 2003 Iraq War.

The perfect script for "when the cannons roar, gold soars."

Gold's response: down 9.5% in one week, wiping out $482 per ounce. The largest single-week dollar decline in the history of gold futures trading. From the all-time high of $5,589 on January 28 to roughly $4,500 at the March 20 close, a drawdown of nearly 20%. If you bought at the top, your "safe haven asset" lost more money than the S&P 500.

The cannons roared. Gold didn't soar. It cratered.

The old saying failed. The question is: why?

You Didn't Buy Gold Insurance. You Bought a Fed Dovishness Derivative.

Understanding this crash requires dismantling a deeply rooted misconception: gold is a war hedge.

It's not. Precisely speaking, gold is a conditional hedge. Dublin City University professors Dirk Baur and Brian Lucey made this condition crystal clear in their seminal 2010 paper: gold can serve as a safe haven during stock market crashes, but in systemic liquidity crises, all assets fall together. No exceptions. In other words, gold insurance has fine print: "This policy may be void when you need it most."

But the real issue goes deeper. Look at every case in the past two decades where gold "successfully hedged," and you'll find the same supporting actor behind each one. His name is the Federal Reserve.

During the 2008 financial crisis, gold dropped from $1,011 to $692, a 33% plunge. But it fully recovered over the following 14 months and gained 166% over three years. Why the rescue? Because the 2008 crisis created deflationary pressure. Prices were falling, so the Fed had to fire up the printing press. Zero rates plus three rounds of quantitative easing pushed real interest rates into negative territory. Gold was the best bet in a negative-rate world.

In 2020, during the pandemic, gold fell 12% in two weeks. Then the Fed unleashed "unlimited QE," and gold recovered all losses within five months, hitting new highs. Same logic: deflationary shock, Fed floods the system, real rates collapse, gold benefits.

The pattern is simple. The prerequisite for gold insurance to pay out has never been "is there a war?" It's always been "will the Fed open the taps?" War is just the trigger. What actually determines whether the policy pays out is whether the Fed has room to cut rates and inject liquidity.

In March 2026, the Fed couldn't cut rates. It definitely couldn't inject liquidity.

On March 18, the Federal Open Market Committee (FOMC) met. Fed Chair Jerome Powell said: "Near-term inflation expectations have risen, likely reflecting sharply higher oil prices driven by Middle East supply disruptions." Then he added: "We are very strongly committed to doing what it takes to keep inflation expectations anchored at 2 percent."

Translation: oil prices are rising, consumer prices are rising, I'm not cutting rates. Trump, give up.

Core PCE was back at 3.0%. The federal funds rate held at 3.5% to 3.75%. Four to five committee members shifted from expecting two rate cuts this year to just one. Futures markets even began pricing in a possible October rate hike, with 50% probability.

This is the paradox at the heart of the 2026 gold crash. Understand this, and everything else falls into place:

You buy gold because you're afraid war will push up prices. But once war actually pushes up prices, the Fed can't cut rates, because cutting would pour fuel on the fire. If the Fed doesn't ease, real rates won't fall. Gold pays no yield; its price rises when real rates decline. Kill that channel, and gold goes nowhere.

The paradox: the very disaster you bought insurance against is exactly what renders the insurance void.

Former Morgan Stanley global currency strategist Stephen Jen coined the "Dollar Smile" theory: the dollar strengthens in two extreme scenarios, one being global panic (capital flees to dollar safety), and the other being US economic dominance (high rates attract capital). The problem in March 2026 was that both sides activated simultaneously. War panic pushed money into dollars. High inflation locked in high rates. The DXY dollar index surged from around 95 back above 100. The 10-year Treasury yield climbed 46 basis points to 4.39%.

Gold is a zero-yield asset. When the dollar is strong and bond yields are high, the opportunity cost of holding gold is, mathematically speaking, devastating. This isn't a "confidence crisis." It's arithmetic.

The King of Safe Havens Is an ATM, Not a Shield

If all you see is "the Fed didn't cut, so gold fell," you're only seeing half the picture. The other half is more dangerous, and it started before the crash.

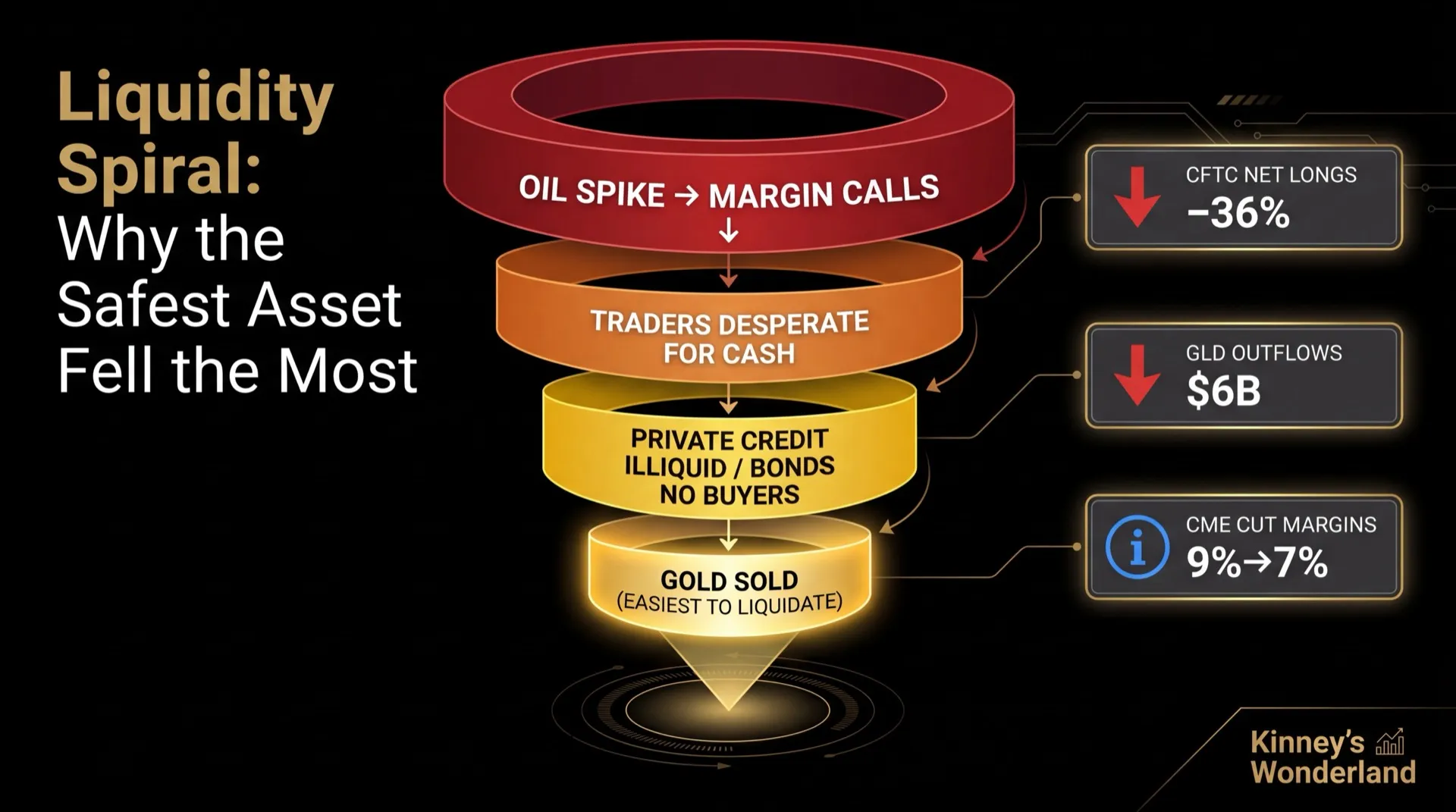

The Commodity Futures Trading Commission (CFTC) publishes weekly positioning reports that show what institutional money is doing. On January 27, gold futures net longs stood at 251,238 contracts. By March 17, that number had dropped to 159,869. A 36% plunge.

In other words, the crash wasn't a sudden event. Institutional players had been reducing positions for seven consecutive weeks starting late January. By mid-March, most of them were already gone. When the bad news hit, there were simply no buyers left.

The world's largest gold ETF, SPDR Gold Shares (GLD), saw over $6 billion in outflows over three weeks, including an 18-tonne single-day redemption on March 4, the largest in GLD's history.

Princeton professor Markus Brunnermeier and London Business School professor Lasse Pedersen proposed a concept called the "liquidity spiral" in 2009. This is exactly what happened:

Oil prices spiked. Exchanges issued margin calls on energy positions. Traders desperately needed cash, but private credit stakes couldn't be sold and corporate bonds maturing in six months had no takers. The things you can liquidate in 30 seconds? There are only a few. Gold is one of them.

People sold gold not because they stopped believing in it. They sold it because it was the easiest thing to sell. In a market where all assets simultaneously need cash, the most liquid asset takes the biggest hit. The king of safe havens isn't a shield. It's an ATM. When you need cash, the ATM is always the first stop.

On March 6, the Chicago Mercantile Exchange (CME) did something counterintuitive: it lowered gold futures margin requirements from 9% to 7%. If gold had crashed due to speculative excess, CME should have raised margins to cool the market, not lowered them. By cutting margins, CME itself acknowledged that this sell-off wasn't a gold-specific problem. It was a chain reaction from the entire market running out of cash simultaneously.

Barchart senior market analyst Jim Wyckoff said: "The Iran War, arguably the biggest geopolitical event in decades, couldn't push gold prices higher. When a market can't rally on bullish news, it means the bull run is over."

Wyckoff wasn't wrong, but he only saw the surface. Gold didn't crash because the bull market ended. It crashed because the entire market ran out of cash at the same time. When markets are uncertain, gold rises, because uncertainty is gold's fuel. But when markets are cash-starved, gold becomes an ATM, and everyone wants to sell it.

But Shanghai Didn't Follow

Wall Street dumped $6 billion in paper gold. COMEX futures prices were in freefall. GLD's net asset value shrank daily.

Then you look at the Shanghai Gold Exchange. The physical gold premium over international prices: positive $30 per ounce.

If the world had truly stopped wanting gold, Shanghai wouldn't have shown a premium. It should have been trading at a discount. But the opposite happened. While Wall Street was panic-selling, Chinese buyers were paying premiums to grab physical gold.

The People's Bank of China had been adding to its gold reserves for 16 consecutive months. Direction unchanged.

The paper market and the physical market were telling two completely different stories. COMEX and GLD told a story about a liquidity black hole and margin calls, starring hedge funds and algorithmic trading. The Shanghai Gold Exchange told a different story, starring central banks and long-term physical buyers, with a simple plot: thanks for the discount.

Pepperstone research strategist Dilin Wu said: "This looks more like a pricing logic adjustment than a long-term trend reversal."

History has always worked this way. In the 1991 Gulf War, gold rose from $384 to $403 when Kuwait was invaded, then fell a net 5.6% after the war ended. In the 2003 Iraq War, gold rose then fell. In the 2022 Russia-Ukraine war, gold spiked briefly then pulled back. Four wars, same script: markets price uncertainty, not violence itself. Uncertainty dissipates faster than the guns go silent.

But 2026 has a structural difference from the previous three. In those cases, Eastern and Western gold markets moved roughly in sync. This time, paper gold and physical gold moved in opposite directions. Wall Street was dumping financialized paper contracts. Asian vaults were absorbing physical bars. The "gold price" as defined by the West was falling. The "gold value" as defined by the East was rising.

After the 2013 "Taper Tantrum," gold fell 28% and took 7 years to recover its highs. After the 2011 peak, it was worse, falling 38% to 44% and taking 9 years to recover. If the 2026 crash is structural, the recovery will be measured in years.

But the bear case has one fatal assumption: Shanghai premiums must turn negative. As long as Asian physical demand continues buying at premiums, the "global gold demand collapse" narrative doesn't hold. Paper gold prices are falling, but physical gold demand hasn't decreased.

If gold fell nearly 10% in one week during the most severe geopolitical military conflict since 2003, the question becomes: in this era, what asset can actually function as a "safe haven"?

The traditional answer is "buy things with intrinsic value."

But March 2026 tells you that when everyone scrambles for cash at the same time, intrinsic value is worthless. In a financial system built on leverage, the definition of safe haven may have already changed: not "what is eternally valuable," but "what won't be the first thing people liquidate when everyone needs cash at the same time."

That question, for now, has no answer.

COMEX paper gold is crashing. Shanghai's physical vaults are buying. Who's right? Today's closing price doesn't have the answer. It lies in the long-term trend of pricing power shifting East.

_(Data sources: WSJ/Dow Jones Market Data, CBS News, TradingEconomics, WolfStreet, FOMC, BanklessTimes, CFTC/TitanFX, Reuters, CME Group, Barchart, Pepperstone. Corrections welcome if any data errors are found.)_

常見問題 FAQ

If gold is a safe haven, why did it crash during a war?

Gold is a conditional safe haven. Its ability to rise depends on the Fed having room to cut rates and inject liquidity. In 2008 and 2020, gold recovered because deflationary pressure let the Fed print money aggressively. In 2026, the Iran War pushed oil prices and inflation higher, preventing rate cuts. With Core PCE at 3.0% and Powell explicitly refusing to ease, real rates stayed elevated, and gold lost its primary upward driver.

COMEX gold crashed but Shanghai premiums hit +$30. What does that mean?

This reflects a split between paper gold (futures, ETFs) and physical gold demand. COMEX selling was driven by hedge fund and algorithmic trading liquidity crises, not a loss of faith in gold itself. Meanwhile, Chinese buyers and central banks continued purchasing physical bars at premium prices. The People's Bank of China added to reserves for 16 consecutive months. As long as Shanghai premiums remain positive, the "gold demand collapse" thesis doesn't hold.

How long could the gold recovery take after this crash?

Historical precedents: gold fell 28% after the 2013 Taper Tantrum and took 7 years to recover; it fell 38-44% after the 2011 peak and took 9 years. The 2026 drawdown from highs is approximately 20%. If the crash is structural (the Fed remains unable to ease for an extended period), recovery could take years. However, if this proves to be a short-term liquidity shock with sustained Asian physical demand, prices may recover more quickly once Fed policy shifts. _—Kinney's Wonderland_