NVIDIA Q4 FY26: Three Hidden Threads, an Earnings Report Nobody Read Right

NVIDIA Q4 FY26 revenue $68.1B beats consensus. Q1 FY27 guidance $78.0B crushes Wall Street. The real story is hiding in DC Networking +267%, Pro Viz +159%, and the China $0 strategy.

This Isn't Another "Beat Again" Article

Two days ago I wrote an NVIDIA preview with two trigger conditions: Q4 revenue above $67B, Q1 guidance above $75B. Less than 48 hours later, both hit — Q4 $68.1B, Q1 guidance $78.0B. After-hours up 3%.

But a 3% move is almost an insult.

The real story in this earnings report isn't the beat itself. It's hiding in three threads Wall Street barely touched: a network cable, a desktop GPU, and a country worth zero. You need to pull out all three threads to see what NVIDIA is actually playing at.

Data Summary

| Metric | Q4 FY26 Actual | Consensus | Beat | YoY |

| --------------------- | -------------- | --------- | -------- | --------- |

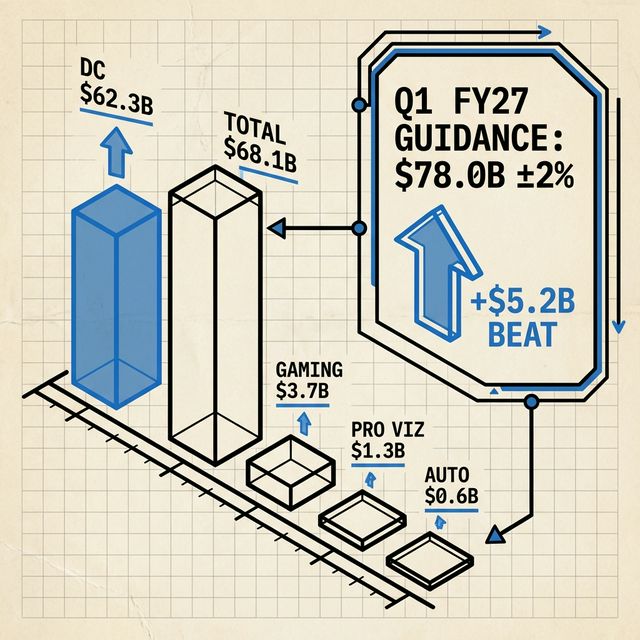

| Total Revenue | $68.1B | $65.9B | +$2.2B | +73% |

| Data Center | $62.3B | ~$58.7B | +$3.6B | +75% |

| Gaming | $3.7B | ~$4.3B | Miss | +47% |

| Professional Viz | $1.3B | $0.77B | +$0.53B | +159% |

| Automotive | $604M | ~$600M | Flat | +6% |

| Non-GAAP Gross Margin | 75.2% | ~75.0% | Hit | +1.7 pts |

| Non-GAAP EPS | $1.62 | $1.53 | +$0.09 | +82% |

| Free Cash Flow | $34.9B | — | — | +125% |

Q1 FY27 Guidance: $78.0B ±2% (consensus $72.8B, beat $5.2B)Pretty numbers. But pretty numbers aren't worth an article. What's worth writing about are the not-so-pretty power plays behind the numbers.

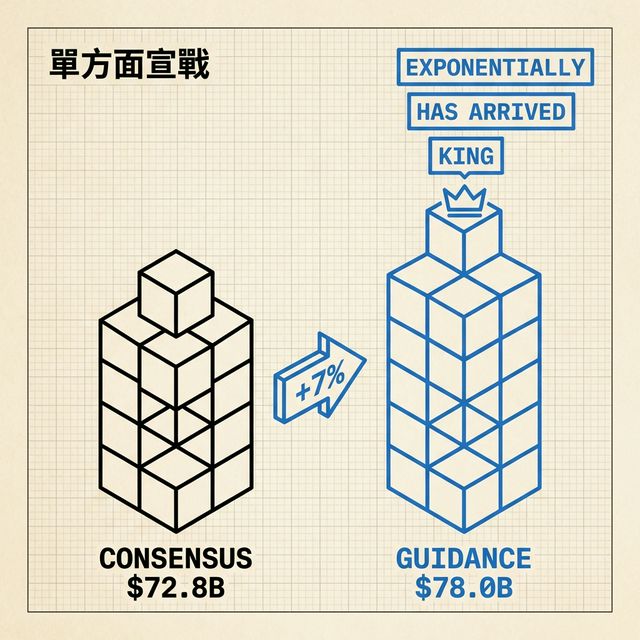

$78B Guidance: This Isn't Expectation Management — It's a Unilateral Declaration of War

Wall Street's consensus for Q1 FY27 was $72.8B. Jensen Huang dropped $78B — 7% higher.

Q4's beat was $2.2B. Q1 guidance beat was $5.2B. The latter is 2.4x the former. But all of Wall Street's headlines were about the former.

Why is guidance ten times more important than actuals? Because Q4's $68.1B is a settled number — channel shipments, customer bookings, analysts tracking it to within a few percent. But $78B is Jensen Huang telling you: the orders in my hand are bigger than the numbers in all of your models.

His exact words:

_"Computing demand is growing exponentially — the agentic AI inflection point has arrived. Grace Blackwell with NVLink is the king of inference today."_

Three words worth unpacking. Exponentially — not "robustly," not "strongly," exponential. Has arrived — not approaching, arrived. King — not "leader" or "best-in-class," but "king." The last time Huang used "king" on an earnings call was 2023, referring to H100. The stock quintupled after that.

And this press release marks the first time Vera Rubin appeared alongside Blackwell. The Rubin platform includes six new chips; after launch, inference costs drop another 10x compared to Blackwell. AWS, Google Cloud, Azure, and Oracle are already in line.

Huang isn't guiding next quarter. He's telling Wall Street: you're still counting beans for this quarter; I'm already designing weapons two generations ahead.

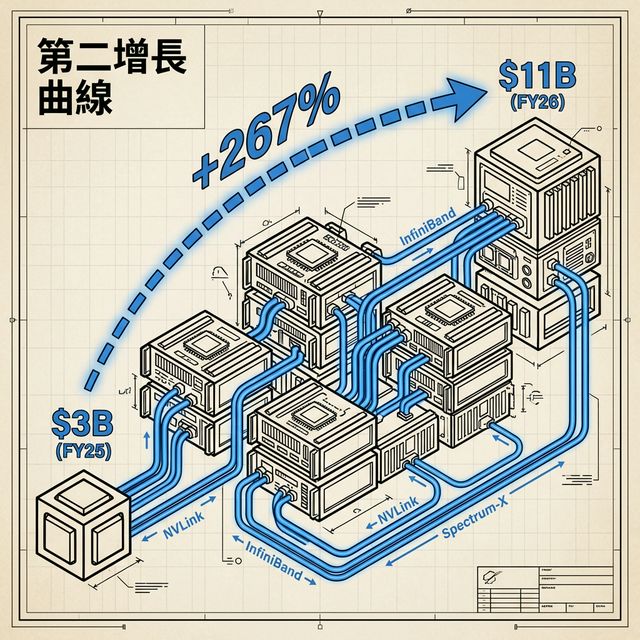

$11B Network Cable: The Second Growth Curve Nobody's Discussing

Everyone saw the $62.3B in Data Center. Break it down:

- DC Compute: $51.3B, YoY +57%

- DC Networking: $11.0B, YoY +267%

267%. A business line at $3B a year ago, quadrupled to $11B in four quarters. Growth rate is triple that of compute itself.

Why does this line deserve its own spotlight? Because it reveals the "second-layer essential demand" of AI infrastructure.

Everyone gets the first layer: buy GPUs, stack compute. But when you cram hundreds of thousands of Blackwell chips into a data center, they need to transfer data at blazing speed — NVLink, InfiniBand, Spectrum-X. These networking interconnect technologies aren't add-on accessories — they're the bottleneck. Without high-speed networking, those GPUs are just very expensive space heaters.

NVIDIA is doing what Microsoft did in the software era. First sell you the operating system (compute), then sell you the Office suite (networking), then sell you Azure (inference platform). The suite's growth often outpaces the operating system itself during the S-curve acceleration phase.

If this line maintains even half its growth in FY27, it'll be approaching $20B by this time next year — bigger than AMD's entire data center division. And in tonight's headlines, almost nobody highlighted this number.

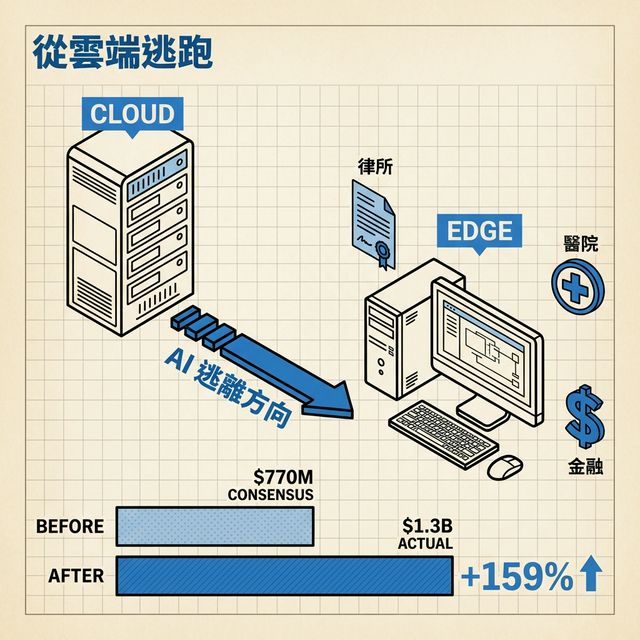

Professional Visualization $1.3B: AI Is Escaping the Cloud

If networking revenue was "overlooked," Pro Viz's numbers were "buried."

Consensus: $770M. Actual: $1.3B. YoY +159%, QoQ +74%.

This isn't linear growth — it's a phase transition. The catalyst is straightforward: the RTX PRO 5000 72GB Blackwell GPU shipped this quarter, designed specifically for running large models and agentic AI workflows on workstations.

Law firms don't want to throw confidential contracts onto the cloud. Hospitals don't want to upload patient records to Microsoft's servers. Financial institutions don't want to add tens of milliseconds of inference latency. So they're putting a Blackwell-chipped workstation under their desks and running models locally. Privacy, latency, cost — three reasons simultaneously pushing AI from cloud to edge.

The result? NVIDIA simultaneously sells you cloud GPUs (Data Center $62.3B), desktop GPUs (Pro Viz $1.3B), and the network connecting them (Networking $11B).

This isn't selling shovels. This is you going to pan for gold, and the road was built by them, the inn was built by them, the gas station is theirs too. And you find there's no way around them.

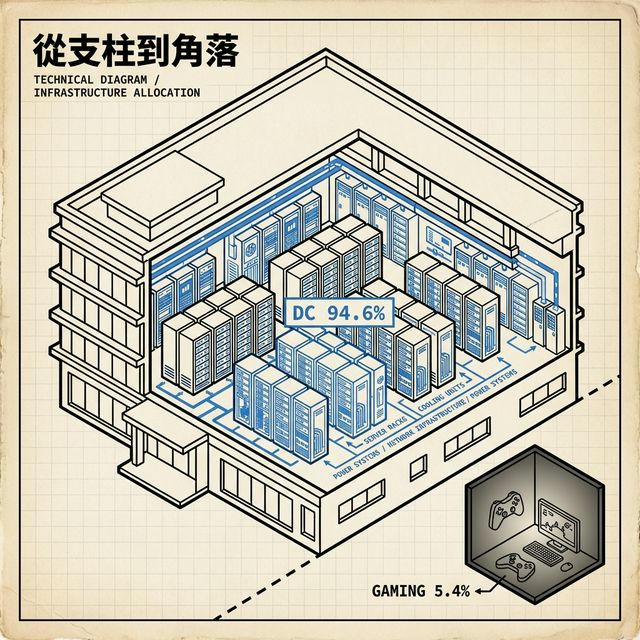

Gaming: From Pillar to Afterthought

Gaming revenue: $3.7B, down 13% QoQ, share shrinking to 5.4%. YoY +47% sounds decent, but that's because last year's base was terrible. Compared to two years ago, this line is basically flat.

RTX 50 series launched at CES in January, but shipments are still ramping and GDDR7 memory supply is tight. The more fundamental issue: production resources have tilted entirely toward data center — engineering headcount, wafer allocation, management attention. Gaming hasn't been eliminated, but it's becoming the forgotten department in a corner of a building.

Anyone still using "NVIDIA is a gaming company" as a valuation framework has been looking at the wrong picture for two years.

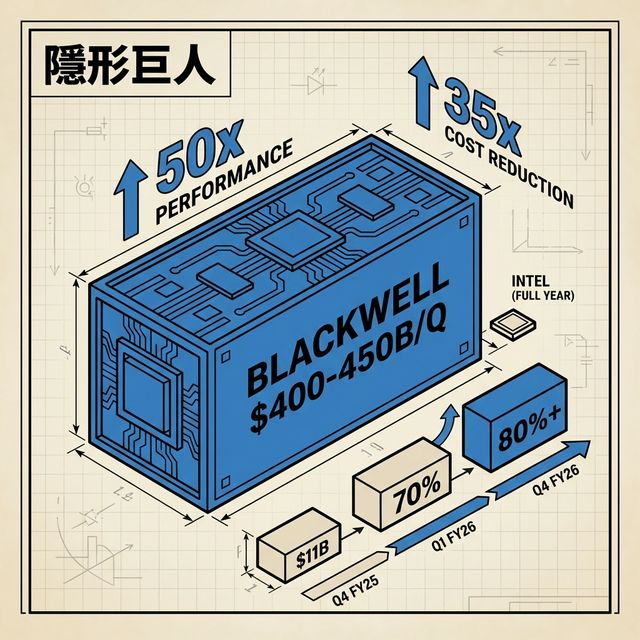

Blackwell: The $40-45B Invisible Giant

NVIDIA didn't disclose Blackwell's specific revenue this quarter. But fragments can be assembled:

- Q4 FY25 (one year ago), Blackwell's first quarter of volume production delivered $11B — Huang called it "the fastest product ramp in the company's history"

- Q1 FY26, Blackwell already represented ~70% of DC Compute

- Q3 FY26, GB300 accounted for roughly two-thirds of Blackwell revenue

- S&P Global estimated full-year FY26 Blackwell revenue at roughly $93.7B

Take Q4's DC Compute of $51.3B, multiply by Blackwell's ~80%+ share (climbing from 70% in Q1), and you land at $40-45B.

One product line. $40-plus billion in a single quarter. This number is bigger than Intel's entire annual revenue.

What's even more terrifying is the next generation. Blackwell Ultra versus the Hopper platform on agentic AI workloads: performance up 50x, cost down 35x. This isn't winning a benchmark by a few percentage points. This is annihilation — the kind backed by SemiAnalysis's InferenceX benchmarks.

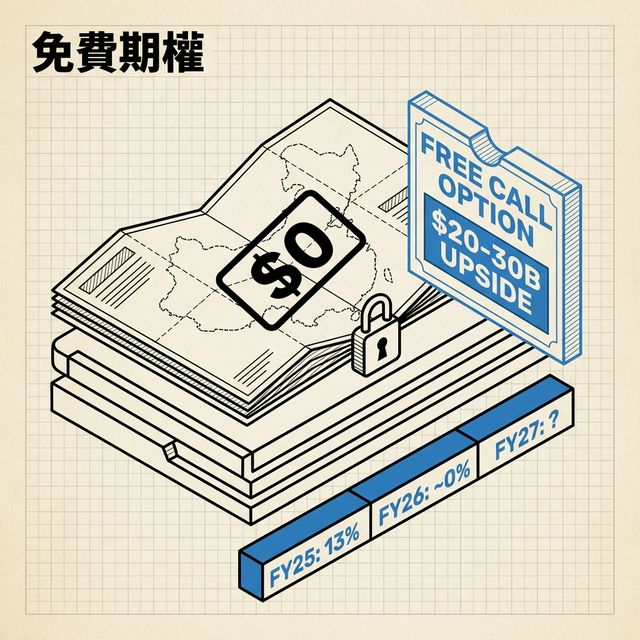

China: A $30B Free Call Option

In Q1 FY27's $78B guidance, China data center compute revenue: zero. Not a penny.

This "$0 China" strategy has been in place for several quarters, but paired with tonight's numbers, the implications sharpen:

China is a free call option. Doesn't need to be modeled, doesn't need to be defended on the call. If U.S.-China relations show the slightest thaw, if the H20 or some downgraded chip gets approved, every dollar that comes in is pure upside surprise.Huang's wording tonight was surgically precise:

_"We're looking forward to returning to China so that we can compete. They have many very strong chip companies, and so we have to compete quite vigorously."_

He chose a safer word — not "sell," but "compete." In Washington's vocabulary, the political distance between those two words is a firewall. And "they have many very strong chip companies" is telling Congress: if you don't let me sell, Huawei and Cambricon will fill that gap, and the one bleeding in the end will be the American semiconductor industry.

In FY25, China accounted for roughly 13% of NVIDIA's revenue. FY26: near zero. If policy cracks open even slightly, $20-30B in annualized revenue could pour in — without building a single factory or hiring a single person.

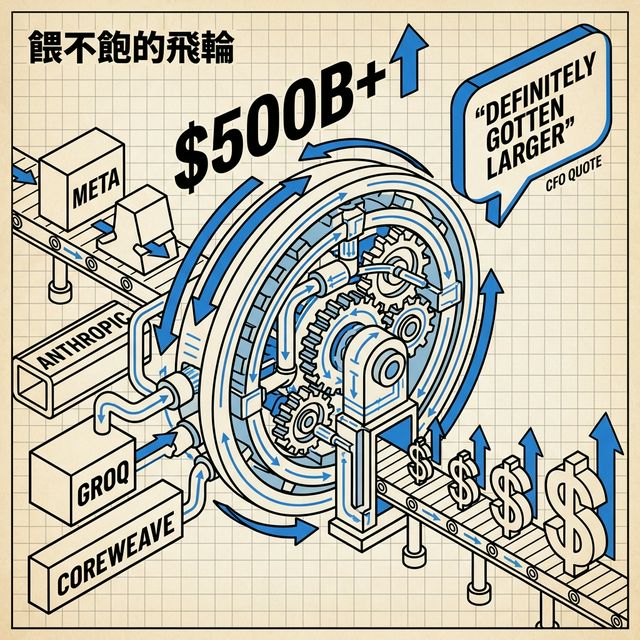

$500B Pipeline: "Definitely Gotten Larger"

In November 2025, Huang disclosed on Q3's call that the Blackwell and Rubin sales pipeline stood at $500 billion, spanning through end of 2026.

In January this year, CFO Colette Kress was asked at a JPMorgan conference whether the number had updated. She said:

_"The $500 billion has definitely gotten larger."_

Tonight's report gave no specific figure. But the press release listed a string of names: Meta multi-year agreement (millions of Blackwell and Rubin GPUs), Anthropic's investment, Groq's licensing deal, CoreWeave's 5+ GW AI factory plan through 2030.

Management choosing not to update the number is itself a chess move. Give a specific number and it becomes a yardstick you can be measured against — don't, and the imagination is limitless. "Definitely gotten larger" — four words more effective than any ten-digit figure at maintaining the market's hunger.

The call also included this: management expects full-year 2026 to see sequential growth every quarter, with magnitude that will "exceed the scope already covered by the $500 billion pipeline." The pipeline is growing, and the velocity of revenue realization is accelerating. This is an insatiable flywheel.

How to Play This Board

Back to valuation.

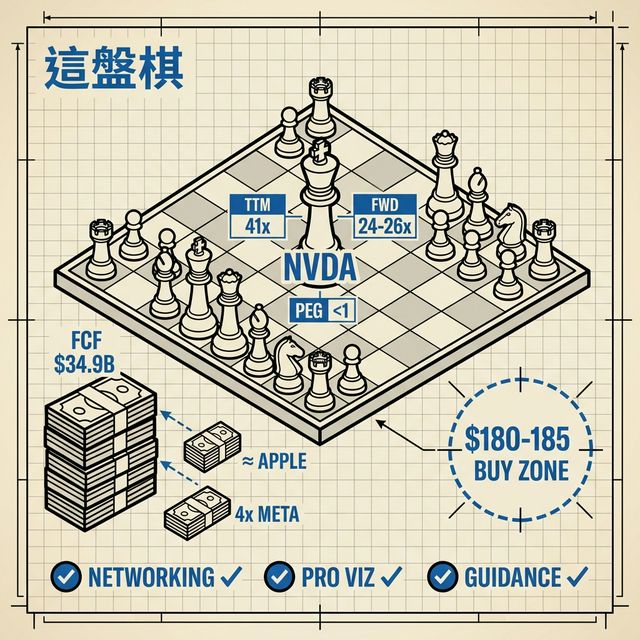

FY26 full-year revenue: $215.9B. Estimated Non-GAAP EPS: ~$4.77. At after-hours ~$196:

- FY26 TTM P/E: ~41x (dramatically improved from 51x two days ago — Q4 EPS boosted the denominator)

- FY27 Forward P/E: if Wall Street revises full-year EPS to ~$7.50-8.00, Forward PE is roughly 24-26x

24-26x. Against 73% revenue growth and 82% EPS growth. PEG ratio well below 1. Among large-cap tech, this isn't expensive — provided you believe growth can continue.

$78B Q1 guidance plus 75% gross margin is practically laying cards on the table: FY27 full-year $300B+ isn't fantasy. Annualizing Q1's $78B midpoint gives $312B. If sequential growth continues (management implied it would), full-year could push to $320-340B.

$34.9B in single-quarter free cash flow. For comparison: Meta's previous quarter FCF was ~$8B; Apple's was just over $30B. NVIDIA's quarterly FCF matches Apple's and is 4x Meta's. Same quarter a year ago: only $15.5B — growth of 125%.

But where's the money going? Q4 buybacks were only $4.1B, half of a year ago's $8.1B, with $58.5B in buyback authorization unused. Plenty of cash but not buying its own stock — NVIDIA closed an approximately $20B acquisition of Groq in December 2025. It doesn't just want to sell GPUs anymore. It wants to control the inference infrastructure platform. Huang is expanding from arms dealer to arms dealer plus base operator.

Short-term: 3% after-hours is far less than this beat deserves. But the past week's broader market pullback already took ~8% off NVIDIA. Tonight's move is less "earnings-driven" than "bottom confirmation." The real buy point isn't tonight — it's if profit-taking over the next few days pulls the price back to $180-185. Long-term: Three new bullets. Networking +267% — second growth curve validated outright. Pro Viz +159% — AI isn't just fighting in the cloud anymore; it's infiltrating every desk — law firms', hospitals', yours. And Q1 guidance 7% above consensus — meaning management's order book exceeds even Wall Street's most optimistic models. Kill switch unchanged: hyperscalers collectively slashing AI Capex, or Blackwell experiencing systemic yield problems. Neither happened tonight. Doesn't mean they never will.The only assumption that needs recalibrating: NVIDIA is no longer "an arms dealer that sells GPUs." It's simultaneously selling networking, selling workstation chips, acquiring inference platforms, and laying out its next two generations' roadmap (Blackwell Ultra → Rubin) right on the table.

This doesn't look like a company worried about hitting the ceiling. This looks like a company that looked at the ceiling and decided to tear off the roof.

Preview Predictions vs. Actual Results

| Prediction Item | Preview Estimate | Actual Result | Verdict |

| ---------------------- | --------------------------- | ------------------- | ----------------------- |

| Total Revenue | $65.6B, beat threshold $67B | $68.1B | ✅ Upside triggered |

| Q1 Guidance | Bull case >$75B | $78.0B | ✅ Far above ceiling |

| Gross Margin Recovery | 75% ±50bps | 75.2% | ✅ Hit |

| Gaming Weakness | ~$4.3B, flat or slight dip | $3.7B, -13% QoQ | ⚠️ Weaker than expected |

| Customer Concentration | Top 4 at 61% | No update disclosed | 🔍 TBD |

| China Zero Assumption | Maintained | Maintained | ✅ |

| After-Hours Movement | Up if both conditions met | Up ~3% | ✅ |

Preview framework was essentially all correct. The only blind spot was Pro Viz's explosion — nobody predicted 159%.

_Sources: NVIDIA Q4 FY2026 official press release, CFO investor presentation, Perplexity Deep Research, prior preview analysis_

_(Data sources: NVIDIA official earnings, analyst consensus compilations. Full earnings call transcript not yet published; certain data points — including specific Blackwell revenue, inference/training split ratio, and updated backlog figures — may be supplemented once transcript is available. Corrections welcome if any data errors are found.)_

_—Kinney's Wonderland_