The Market May Be Making Its Biggest Pricing Error Since 1983

WTI surged 35% in one week — Wall Street is pricing a 4-week war. But a collapsed insurance market, saturated storage facilities, and a mine-clearance capability gap have created a commercial deadline that no politician's social media post can resolve.

On March 6th, the electronic sign at a Shell station in San Jose, California flashed $7.09 a gallon. The middle-aged man standing by the pump snapped a photo and posted it on X. Thirty thousand reposts in fifteen minutes. Someone commented: "I didn't see this number even during the 2008 financial crisis."

What he didn't know was that seven dollars was still cheap.

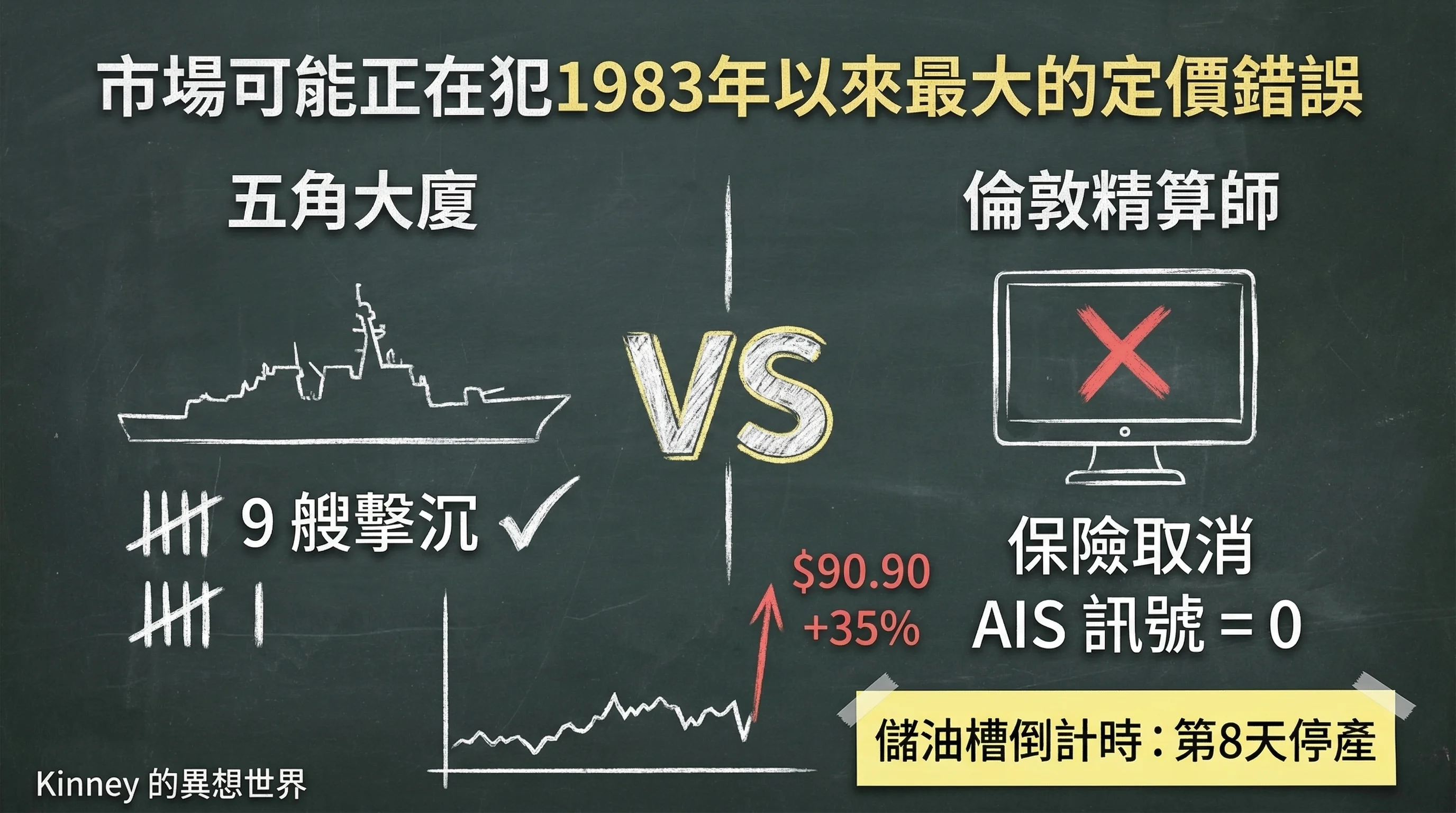

That same day, West Texas Intermediate (WTI) closed at $90.90, up over 12% in a single session. The weekly gain: 35.63% — the largest one-week surge since crude oil futures began trading in 1983. Brent closed at $92.69. U.S. Energy Secretary Chris Wright reassured reporters that oil prices would come down "in weeks, not months." The same day, President Donald Trump posted on Truth Social demanding Iran's "unconditional surrender."

History's most famous demand for unconditional surrender came at the 1943 Casablanca Conference, when President Franklin Roosevelt delivered it to the Axis powers. From that utterance to Japan's actual surrender took 2 years and 7 months — and two atomic bombs.

The Energy Secretary says weeks. But wars fought under the banner of "unconditional surrender" have never wrapped up in weeks. These two sentences come from the same government, contradicting each other with such candor that the speakers might as well inhabit different universes.

And the market? The market slapped a roughly $13-to-$18-per-barrel "war risk premium" on all of this. In plain English: Wall Street thinks this war wraps up in about a month.

I believe this may be the biggest pricing error since 1983.

The U.S. Navy Won Every Battle, but the Strait Is Zero

Let's start with the good news. Operation Epic Fury's first week was a military textbook. Nine Iranian naval vessels sunk, including a Jamaran-class frigate. A submarine torpedo sank the Iranian frigate IRIS Dena — the first U.S. submarine torpedo kill since World War II. The 42,000-ton drone carrier Shahid Bagheri was sent to the ocean floor. U.S. Central Command (CENTCOM) declared the Strait of Hormuz "not closed."

Then you look at the shipping data. At midnight on March 2nd, AIS vessel signals in the Strait of Hormuz dropped to zero. Not low. Zero.

The world's four largest shipping giants — Maersk, Hapag-Lloyd, CMA CGM, and Norden — all suspended operations and rerouted around the Cape of Good Hope, adding 15 days to each voyage. Over 150 oil tankers sat stranded on the open seas outside the Persian Gulf, like a convoy of billion-dollar trucks stopped at a toll booth.

The U.S. Navy didn't lose a single battle. Shipping through the Strait of Hormuz: zero.

How do you explain this contradiction? The answer isn't in the Pentagon. It's in the City of London.

On March 5th, seven of the world's largest marine mutual insurers — including Norway's Gard, the UK's NorthStandard, and the London P&I Club — formally cancelled all war risk and P&I coverage for Persian Gulf routes within 72 hours. An uninsured vessel cannot leave port — that's a hard rule in international maritime law. It's not that captains are afraid to sail; the law literally prohibits it.

What determines whether the Strait of Hormuz is navigable isn't the U.S. Fifth Fleet's aircraft carriers. It's the risk model running on a London actuary's computer.

A $200 Billion Rubber Check

The White House response was creative: drag in the U.S. International Development Finance Corporation (DFC) to provide up to $200 billion in war risk reinsurance.

What is DFC? Its predecessor was the Overseas Private Investment Corporation (OPIC), reorganized in 2019 with a statutory mission to counter China's Belt and Road Initiative. Its normal business is insuring American companies building power plants in Kenya against political risk. Fixed, land-based, immovable assets. Now it's being asked to underwrite supertankers shuttling through a mine-infested Persian Gulf.

The arithmetic is simple. A fully loaded VLCC supertanker: hull value approximately $120 million, carrying 2 million barrels of crude at $90 per barrel worth $180 million. Ship plus cargo: roughly $420 million per claim. And that's before oil spill cleanup — the Exxon Valdez alone cost over a billion in 1989. DFC's $200 billion? Five to ten sinkings would blow through it.

But money isn't even the most lethal problem. DFC has zero marine claims adjusters on staff. Lloyd's of London's maritime claims ecosystem has been operating for three centuries. DFC's employees are economists and lawyers in a Washington office. DFC enjoys sovereign immunity; policies must include stringent terms: vessels must strictly follow routes designated by CENTCOM. Captain deviates one nautical mile to dodge a mine and gets hit? Washington's lawyers can — and will — invoke "breach of contract terms" to deny the claim. Shipowners can't win against the U.S. federal government.

The more fundamental issue is timing. This plan was cobbled together between March 3rd and 5th — not a pre-war contingency plan, but something jury-rigged five days after the war started. The R Street Institute, a U.S. think tank, pointed out that DFC's own website lists Iran as an "unsupported country."

As of this writing, the number of commercial vessels that have transited the Strait of Hormuz using DFC insurance: zero.

The world's top financial institutions have determined that the risk in these waters is "uninsurable." When a free-market government is forced to become the insurer of last resort, that's not a display of power. That's a letter of surrender.

The Pentagon Knew This Would Happen — 24 Years Ago

In July 2002, the Pentagon spent $250 million on a massive war game called Millennium Challenge 2002. The scenario: U.S. forces versus a Persian Gulf state, widely understood to be Iran. The Red Team commander was retired Marine Corps Lieutenant General Paul K. Van Riper.

Van Riper used asymmetric tactics: cruise missiles combined with swarms of suicide small attack boats. Within minutes, he simulated "sinking" 16 U.S. warships, including an aircraft carrier, with approximately 20,000 simulated casualties.

The Pentagon's response: pause the exercise. "Refloat" the sunken ships. Restart. Then restrict the Red Team's freedom of action to ensure a Blue Team victory.

Van Riper publicly denounced the exercise as "scripted," saying the military squandered the chance to learn painful but critical lessons. The Pentagon chose not to change its strategy — it changed the rules.

Twenty-four years later, Iran is using precisely the concept Van Riper predicted — just with upgraded weapons. In 2002, it was boat swarms and cruise missiles targeting warships. In 2026, it's drone swarms and unmanned surface vessels targeting commercial ships, plus ballistic missiles hitting military installations. Same concept, broader attack surface, lower cost.

There's only one difference. In 2002, the Pentagon could hit the pause button and refloat its ships. In 2026, there is no pause button.

The Storage Tank Countdown to Death

How does Wall Street see all this? Goldman Sachs head of oil research Daan Struyven used a mathematical concept rare on Wall Street: convex function.

In plain language: the oil price shock isn't proportional. If the Strait is disrupted for two weeks, oil sits in onshore storage — minimal impact. But past a certain threshold, prices don't climb a slope; they shoot straight up.

Where is that threshold? JPMorgan's global head of commodities strategy, Natasha Kaneva, provided the countdown. Persian Gulf producers have approximately 343 million barrels of onshore storage capacity in the Hormuz-dependent zone. Sounds substantial — but this isn't an interconnected system. Iraq and Kuwait have far smaller storage facilities than Saudi Arabia.

Day 8: Iraq and Kuwait's storage hits capacity. Oil can't ship out, can't be stored on land — wells are forced to shut in. Approximately 3.3 million barrels per day of production capacity goes offline.

Day 18: Forced shutdowns rise to 4.7 million barrels per day.

Around Day 25: the entire system saturates.

These three numbers mean one thing: storage tanks don't wait for diplomatic negotiations.

Iraq's giant Rumaila oil field is already demonstrating Step One. Imagine the control room of this superfield producing 1.5 million barrels daily: pressure curves going red on screen, one after another. Crude can't ship out, onshore facilities at capacity, water injection pumps and rod pumps must shut down simultaneously. The engineers watch the numbers, knowing exactly what comes next, powerless to stop it.

Most people assume oil fields work like faucets — turn off, turn back on. They don't.

A mature waterflood field like Rumaila, producing for over 70 years, exhausted its natural reservoir pressure long ago. It relies entirely on injecting millions of barrels of water daily to maintain pressure equilibrium, "squeezing" the crude out. Once forced into emergency shutdown, injection pumps and rod pumps halt simultaneously, and the dynamic oil-water pressure balance maintained for decades collapses. Groundwater reverse-infiltrates and seals oil-bearing pores. Wellbore temperatures drop, causing massive precipitation of wax and asphaltenes that clog micron-scale rock fractures. Like blood clots blocking capillaries.

Energy consultancies Rystad Energy and Wood Mackenzie issued specific warnings during the 2020 COVID production shutdowns: unplanned shutdowns of mature waterflood fields typically result in permanent initial production losses of 5% to 15%. Not temporary. Permanent.

When the Strait reopens and the valves turn, what comes out could be up to 80% water. To revive a well requires either continuous coiled tubing chemical washes or drilling new sidetracks. Some marginal wells are simply written off.

Assuming Kuwait plus southern Iraq undergo full shut-in for one month at a conservative 8% permanent damage rate, the global crude market would permanently lose approximately 450,000 barrels per day of base production capacity. These 450,000 barrels represent OPEC+'s most core, lowest-cost genuine spare capacity.

Wall Street's Excel models contain an assumption called "full post-war production recovery." Physics has a two-word answer to that assumption: not possible.

So the question isn't "when does the oil price come back down." It's "where is the floor when it does." The answer: permanently $10 to $20 higher than pre-war levels.

"Unconditional Surrender" Meets the Impossible Trinity

Now back to those two contradictory statements.

The Energy Secretary says weeks. The President says unconditional surrender. Historically, every leader who demanded unconditional surrender inadvertently made a decision for the other side: since surrender means death anyway, at least fighting buys time. Some historians argue that Roosevelt's unconditional surrender demand itself prolonged World War II by eliminating the opponent's exit ramp — leaving them to choose between "death" and "death."

And the market is pricing a 4-week war.

OPEC+ has approximately 3.5 million barrels per day of theoretical spare capacity, primarily in Saudi Arabia and the UAE. The problem: those barrels must pass through the Strait of Hormuz to reach buyers. Wood Mackenzie used a precise description: "dual supply shock." What makes 2026 unique isn't just that existing exports are severed — even OPEC's theoretical spare capacity is physically trapped inside the Persian Gulf. Global buyers literally cannot access it. There is no historical precedent.

Pre-war market consensus was bearish on oil. Weak Chinese demand, strong non-OPEC production, structural oversupply in 2026. JPMorgan's own full-year forecast had Brent averaging $50 to $60. Precisely because of this bearish consensus, large numbers of hedge funds and CTAs had built net short positions. When military strikes plus the Strait blockade hit, prices blew through one technical resistance level after another, automated trading systems triggered margin calls, and mechanical short-covering kicked in. In energy trading parlance: a classic commodity short squeeze. The pace of the rally was driven by panic, not fundamental valuation.

Then came the second-order effects. Quieter than missiles, deadlier than missiles.

Morgan Stanley's estimate: every 10% increase in oil prices pushes the Consumer Price Index up 0.35 percentage points within three months. Every 25-cent rise in gasoline reduces real retail spending by 0.7%. On March 6th, the national average gasoline price hit $3.32 per gallon, surging 11.4% in one week. Individual stations in California breached $7.

Airline stocks were cratering. American Airlines fell 4.2% in a single day. Deutsche Bank used the phrase "existential threat" to describe oil's impact on the airline industry. Carnival Cruise dropped 12%. Fuel accounts for 20% to 30% of airline operating costs. They have no pricing power.

February's non-farm payrolls, reported on March 6th, collapsed to negative 92,000. Consensus had been positive 50,000. The economy was already deteriorating while oil prices kept climbing.

The Federal Reserve is trapped in an impossible trinity. It can't cut rates because energy is pushing prices higher. It must cut rates because employment is collapsing. This combination has a name. The last time it appeared was after the 1973 oil embargo. Stagflation.

BMI, a Fitch Ratings subsidiary, forecasted: the oil price surge could shave 0.1 to 0.3 percentage points off major economies' real GDP while pushing headline inflation up 1.0 to 2.5 percentage points.

Who pays? The driver commuting in California. The family booking spring flights. The pension fund holding airline stocks. Every entity in the inflation transmission chain without pricing power.

Punishing One Dictator, Feeding Another

On March 6th, Treasury Secretary Scott Bessent announced a partial relaxation of Russian oil sanctions, authorizing India to purchase stranded Russian oil and lifting sanctions on Rosneft's German subsidiary. His stated rationale: to "create supply" and "ease the pressure caused by Iran's attempt to hijack global energy."

Translation: to punish the theocratic thugs in Tehran, the U.S. was forced to pump blood into the dictator in Moscow.

Russian Deputy Prime Minister Alexander Novak sensed opportunity, announcing plans to redirect LNG exports from Europe to China and India, jumping into the global gap left by Qatar's LNG shutdown. The result? Moscow and Beijing secure energy first; Western allies absorb the shortage. Bessent's "creating supply" was essentially an admission of a brutal arithmetic: you cannot simultaneously unplug two major oil-producing authoritarian regimes and expect inflation to soft-land.

The War Powers resolution failed in the Senate 47-53, introduced by Democratic Senator Tim Kaine, in a nearly party-line vote. The sole Republican to vote in favor was Senator Rand Paul, who said: "Congress should be ashamed for allowing this unilateral war." It failed in the House 212-219. House Speaker Mike Johnson's quote: "We are not at war. The mission is nearly complete."

The Pentagon is bombing Iranian missile installations daily. The Speaker says we're not at war. This degree of deliberate cognitive dissonance means there are no institutional brakes. The war's duration is determined by one man's mood.

When asked about oil prices at a press conference, Trump replied: "If they rise, they rise. I'm not concerned."

Put it together: no Congressional check, plus a president openly indifferent to economic consequences, plus an "unconditional surrender" demand contradicting the White House's own "4-to-6 weeks" estimate. The market's assumed "rational exit" has zero institutional foundation.

Three Counterarguments You'll Hear

"Can't we just release the Strategic Petroleum Reserve?"The U.S. Strategic Petroleum Reserve (SPR) currently holds approximately 415 million barrels, with a maximum daily drawdown of 4.4 million barrels. The Strait of Hormuz disruption affects nearly 20 million barrels per day. Using the SPR is like fighting a forest fire with a garden hose. And the SPR was already drawn down heavily during the 2022 Russia-Ukraine war — current inventory is far below its 714 million barrel capacity.

"There are alternative pipelines that bypass the Strait."The Saudi East-West Pipeline plus the Abu Dhabi pipeline have combined available remaining capacity of roughly 3.5 million barrels per day. Sounds significant? The Strait of Hormuz normally handles 20 million barrels daily. You've blocked the main artery and expect capillaries to sustain the body's entire blood circulation. Alternative pipelines can save lives, but they can't save the market. A 15-million-barrel gap remains locked inside the Gulf.

"Trump will declare victory and withdraw — he's transactional like that."I'll concede the possibility. Trump does possess an extraordinarily transactional personality, and his political U-turn speed is unmatched globally. But even if Trump announces a peace deal on Truth Social tomorrow, Iran's stockpile of 5,000 to 6,000 naval mines won't vanish because of a post. That's the Defense Intelligence Agency's (DIA) estimated inventory — stockpile, not deployed count. But insurance companies don't look at politicians' social media; they look at whether minefields have been cleared.

And the Persian Gulf's mine-clearance capability? The dedicated Avenger-class minesweepers were fully decommissioned in September 2025. The replacement Littoral Combat Ships (LCS) with mine countermeasure modules have, according to a Government Accountability Office (GAO) assessment, an operational availability rate of just 29%. Towed array brackets fracture, unmanned surface vessel recovery fails, sonar resolution degrades in the Gulf's turbid waters. Full clearance is estimated at 4 to 8 weeks — and that's the optimistic version.

There's an even more insidious technical detail: Iran's new-generation mines are equipped with electronic "ship counters." They let minesweepers and unmanned vessels pass safely. They detonate only when the second or third large commercial vessel transits. Meaning: after mine clearance vessels declare the area "safe," commercial ships can still hit mines.

Politics can U-turn in a second. Minesweepers cannot.

Seven Dollars Is Just the Beginning

The 1973 oil embargo was an administrative decision by the Organization of Arab Petroleum Exporting Countries (OAPEC) — it could be ended at the negotiating table. The 1990 Gulf War had a clear military objective: liberate Kuwait, fight, leave. The 2022 Russia-Ukraine war's oil price shock was primarily sanctions-driven — shadow fleets could circumvent them, and the Strait of Hormuz stayed open throughout.

2026 is a three-in-one. The supply disruption of 1973, plus the direct U.S. military involvement of 1990, plus the algorithmic market structure of 2022. And it adds an element that has never appeared in history: the physical blockade of the Strait of Hormuz. Not an administrative decree. Not sanctions compliance. It's a collapsed insurance market, plus mines, plus a mine-clearance capability gap — all three forming a commercial deadline.

Helima Croft, head of global commodities strategy at RBC Capital Markets, explicitly warned of the market's "recency bias": don't use the brief conflict in June 2025 to predict this one. Iran may adopt a completely different attrition strategy. Goldman Sachs' Struyven said it too: "How long the Hormuz disruption lasts is the single most important variable in today's market."

The problem is that no financial analyst has an information edge on this variable. Whether the Strait reopens in days or remains blocked for months depends on IRGC decision-making, Trump's war objectives, and whether a ceasefire mechanism emerges. None of these are things financial models can predict.

You can start a war in one day. You cannot, in one day, get a London actuary to check the box marked "navigable." Don't watch the White House victory speech. Watch the London actuary's screen. Don't count the U.S. military's missile inventory. Count Kuwait's remaining storage tank capacity. Because in this war, winning requires firepower — but keeping the world running requires insurance and logistics. And neither takes orders from politicians.

Next time you see $7 at a California gas station, remember: the actuary hasn't checked the box yet.

常見問題 FAQ

Why is the Strait of Hormuz still impassable despite a U.S. military "victory"?

Because navigability isn't determined by the military — it's determined by the insurance market. On March 5, 2026, seven of the world's largest marine mutual insurers cancelled all war risk coverage for Persian Gulf routes within 72 hours. Under international maritime law, uninsured vessels cannot leave port. The U.S. emergency DFC $200 billion reinsurance program has seen zero commercial vessel usage as of March 7.

How would a sustained oil price shock impact ordinary consumers?

According to Morgan Stanley, every 10% increase in oil prices pushes the Consumer Price Index up 0.35 percentage points within three months. Every 25-cent rise in gasoline reduces real retail spending by 0.7%. The U.S. national average gasoline price hit $3.32 per gallon on March 6, 2026, surging 11.4% in one week. BMI (Fitch Ratings) forecasts that the oil price surge could push headline inflation up 1.0 to 2.5 percentage points.

Why might the assumption of "oil prices returning to pre-war levels" be wrong?

Because forced well shut-ins cause permanent damage to mature oil fields. Rystad Energy and Wood Mackenzie warned in 2020: unplanned shutdowns of mature waterflood fields typically result in 5% to 15% permanent production loss. If Kuwait plus southern Iraq undergo full shut-in for one month at an 8% permanent damage rate, the global market permanently loses approximately 450,000 barrels per day of base production capacity.