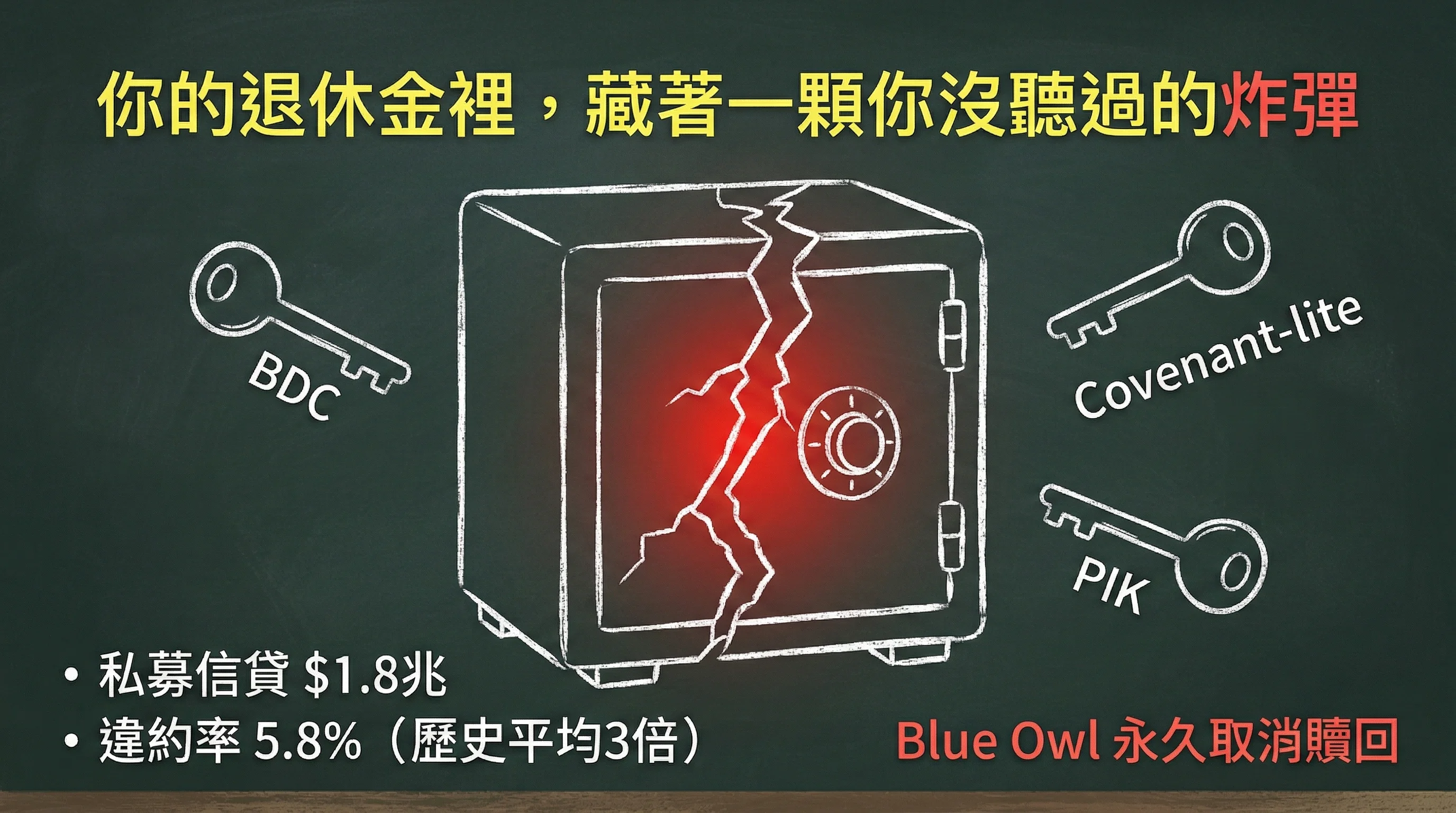

There's a Bomb Inside Your Retirement Fund That You've Never Heard Of

The $1.8 trillion private credit market's default rate just spiked to 5.8% — triple the historical average. Blue Owl Capital permanently canceled fund redemptions, selling the best assets to insurance companies. Your 401k, annuities, and universal life policies may be holding these things. Know what you own.

Open your 401k account. Find the "alternative investments" section, click in, and look for "private credit," "direct lending," or a bunch of abbreviations you don't understand.

There's a good chance it's there.

You think you only hold a few ETFs and tech stocks. But your retirement fund, annuities, and universal life insurance are holding something on your behalf that you've never even heard of. As of January 2026, the default rate on this stuff just spiked to 5.8% — triple the historical average.

This article doesn't predict a crash. What I'm going to do is very simple: tell you where your money is.

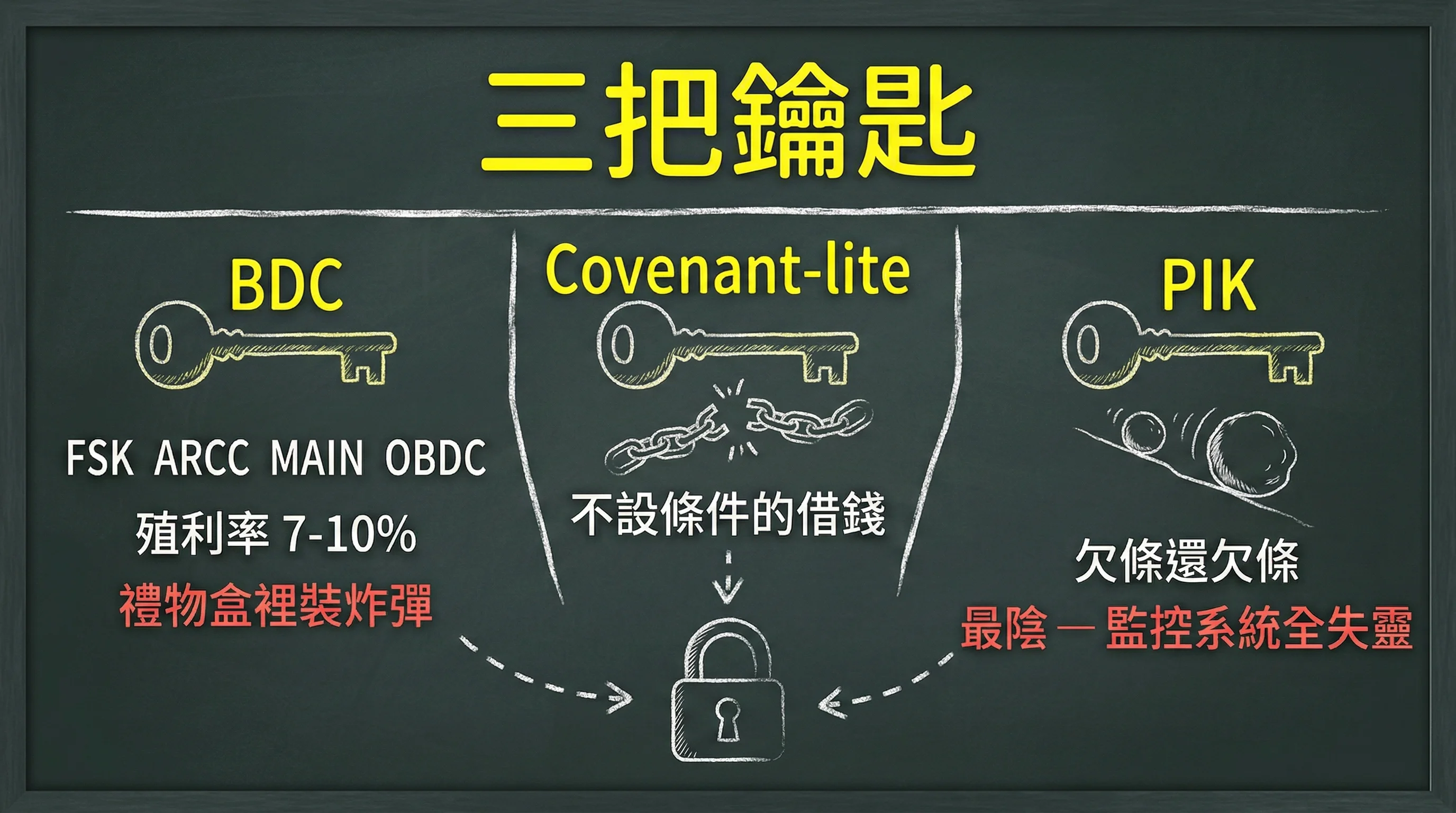

Three Keys

The entire private credit game can be summarized in three terms.

First, the one you're most likely to encounter: BDC (Business Development Company). Pull up your brokerage platform and search FSK, ARCC, MAIN, OBDC — those are all BDCs. Yields of 7% to 10%, looking like a gift from heaven. The price is that you're not eating interest — you're eating the premium on credit risk. Inside the gift box is a bomb.

The second term is Covenant-lite — in plain English, "lending with no strings attached." Traditional lending comes with strict restrictions: leverage ratios, cash flow coverage multiples, all with red lines. Covenant-lite strips away all the red lines. Nobody cared during the zero-rate era. When rates went up, the pain arrived.

The last one you need to remember is PIK (Payment-in-Kind). This one's the most insidious. Borrowers don't pay interest in cash — they pay with IOUs on top of IOUs. On paper, no defaults ever occur, but underneath, debt metastasizes like cancer. You see a pretty number in the quarterly report; behind that number is an ever-thickening stack of IOUs. Why is it the most insidious? Because it renders every monitoring system blind: default rate data can't see it, until the snowball grows large enough to crush everything.

These three terms are the hole cards of the entire game.

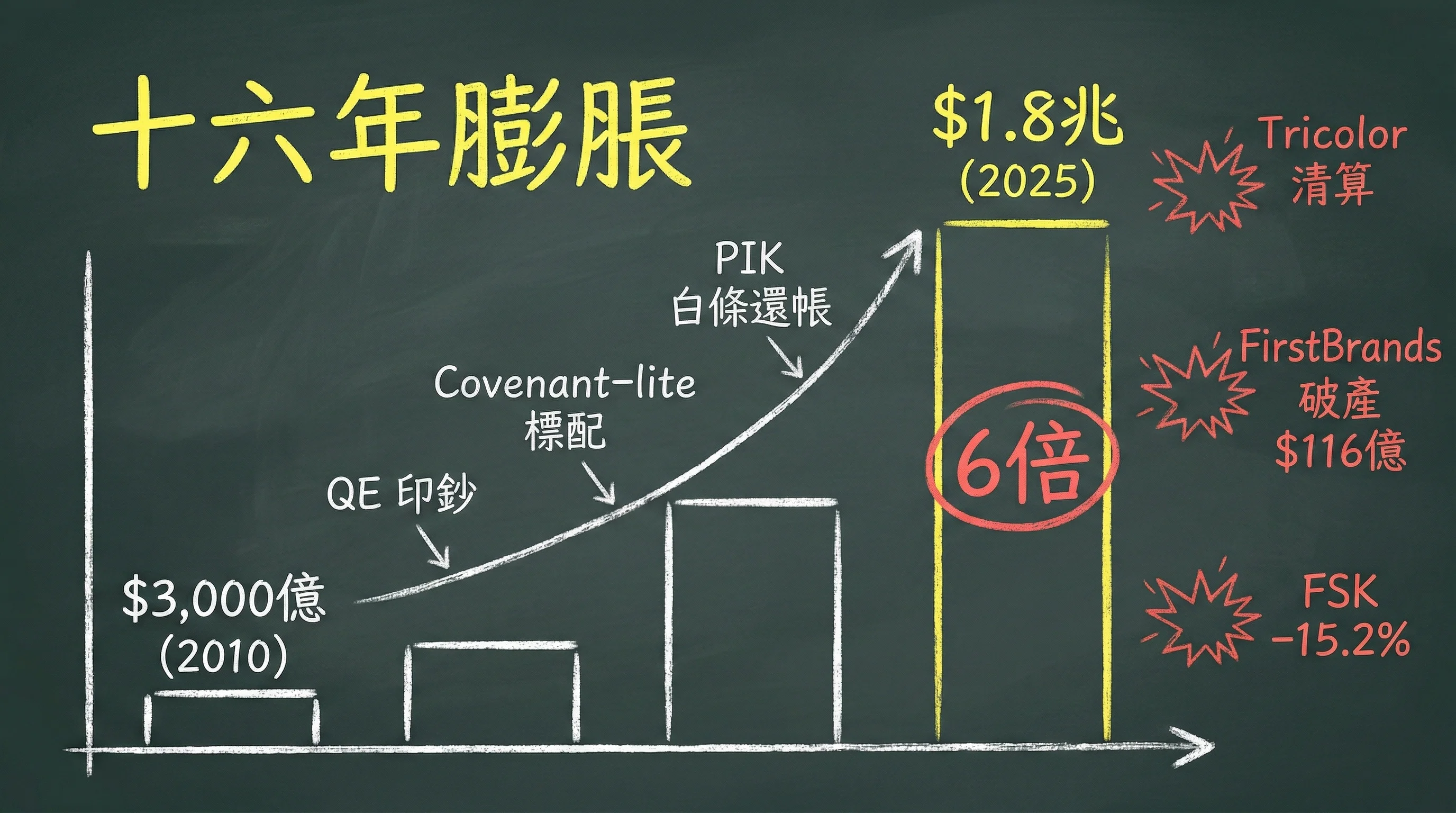

From $300 Billion to $1.8 Trillion: A Sixteen-Year Slow-Motion Expansion

After the 2008 financial crisis, regulators used Dodd-Frank and Basel III to slash banks' lending capacity. Companies still needed to borrow, and if they couldn't borrow from banks, they'd borrow elsewhere. Private credit funds filled that hole, attracting capital with high yields. In 2010, the entire market was about $300 billion; by the end of 2025, it had ballooned to $1.8 trillion. Six times.

During the QE money-printing era, money everywhere was chasing yield. Private credit drew it in with 7% to 9% returns, accelerating ever faster, discipline loosening ever more. Covenant-lite became standard, and PIK let borrowers pay with IOUs.

Then the mines started detonating. September 2025: Tricolor liquidated. Same month, FirstBrands filed for bankruptcy with $11.6 billion in liabilities and $2.3 billion in fabricated receivables. Early 2026, FS KKR slashed its quarterly dividend by 30%, from $0.64 to $0.45. The stock plunged 15.2% that day.

But what made the entire industry take notice was what Blue Owl Capital did.

Dissecting Blue Owl's Week

Blue Owl's management told investors: "We think this is a difficult short-term patch."

Then did three things.

First: permanently canceled quarterly redemptions for OBDC II. Not suspended — permanently canceled. The rules were rewritten. You entered the fund because of the words "quarterly redeemable." Now the door is shut and the rules have changed. You'll receive $2.35 per share by end of March — about 30% of net asset value. The remaining 70% is locked in the fund, waiting for underlying loans to mature. When will they mature? Nobody tells you.

Second: sold $1.4 billion in loans. The buyers were North American pension funds and insurance companies. Transaction price: 99.7% of face value — looks like market price.

Third: what they sold was the best assets in the portfolio. Pension funds and insurance companies got the cream. The investors locked in the fund are holding what's left after the cream is skimmed. Quality? Nobody knows, because these assets are valued using mark-to-model — the fund manager decides what they're worth.

BDCs are the conduit, Covenant-lite is the borrower's talisman, PIK is the cosmetics covering up the truth. Three keys, turned together — that's what happened during Blue Owl's week.

The Causal Chain: How It All Connects

Step back one level upstream.

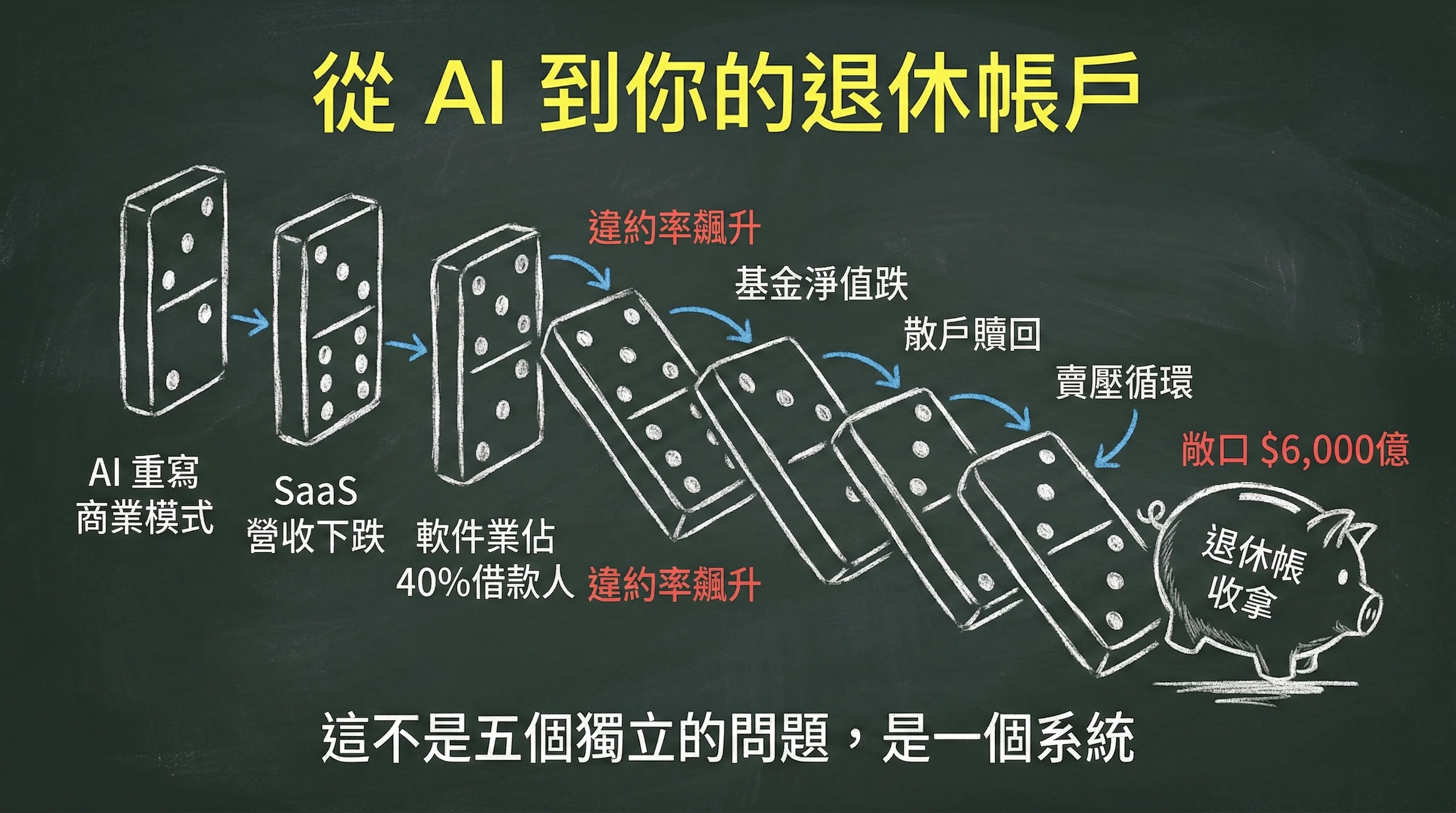

Why is it blowing up now? Private credit has been expanding for sixteen years — why are things going wrong in 2026?

Because AI is rewriting the business model of the software industry. Not the "machine awakening" sci-fi storyline — this is real revenue impact. A SaaS company lives on enterprise subscription fees: a client pays $100,000 a year for data analytics. Now the client discovers Claude or GPT can do the same thing in seconds for $20 a month. Subscription canceled. Not one company — an entire industry is recalculating.

Where's the problem? Software companies account for roughly 40% of private credit borrowers. Exposure exceeds $600 billion.

AI compresses these companies' cash flows → borrowers can't repay → default rates spike from the historical average of 1-2% to 5.8% → fund NAV drops → retail investors demand redemptions → fund managers forced to sell assets → selling pressure pushes NAV down further.

You thought AI panic was just a sci-fi topic. It's not. It's a financial transmission chain: tech-side business model collapse, transmitted through the credit pipeline, into your retirement account.

These aren't five separate problems. It's one system.

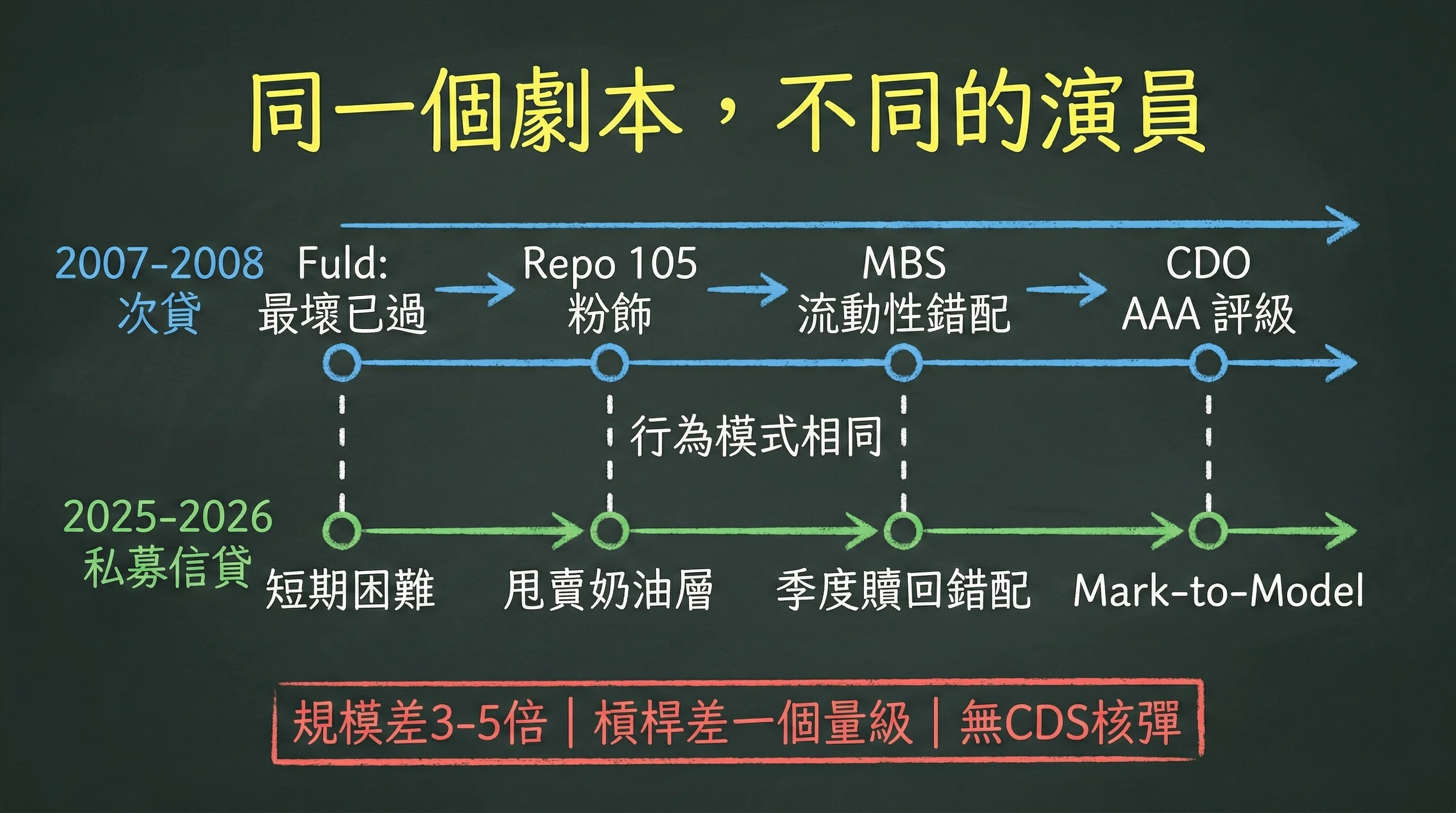

Same Playbook, Different Actors

Place 2007-2008 and 2025-2026 side by side, and you'll notice something unsettling: the behavioral patterns are nearly identical.

Management denial. Lehman Brothers CEO Richard Fuld told shareholders in April 2008: "The worst is behind us." Five months later, Lehman filed for the largest bankruptcy in U.S. history. Blue Owl says "short-term difficulty." Different words, same playbook.

Asset transfer window-dressing. Lehman used Repo 105 to temporarily "sell" $50 billion in assets to counterparties, buying them back after quarter-end reporting — instant balance sheet leverage improvement. Blue Owl sells $1.4 billion in prime loans to insurance companies at "market price" of 99.7%. One is quarter-end magic; the other is dumping the cream layer. Different operations, same logic: keeping investors from seeing the bad stuff.

Liquidity mismatch. In 2008, MBS was packaged as "highly liquid" products; the underlying assets were 20-30 year mortgages. Today, private credit funds attract retail investors with "quarterly redemptions"; the underlying assets are completely illiquid private enterprise loans. When everyone demands redemption at once, the fund manager can't sell what's in hand.

Valuation distortion. Moody's and S&P gave CDOs AAA ratings. Today, private credit uses mark-to-model valuation. You see a number in the quarterly report — nobody can confirm that number reflects real value.

But let me be clear about the differences too. Scale differs by 3-5x: the 2007 MBS market was $5.8 trillion; private credit is $1.8 trillion. Leverage differs by an order of magnitude: investment banks then ran 30-40x; private credit borrowers operate at 5-5.5x EBITDA. Most crucially, 2008 had CDS — the derivative amplifier with notional value exceeding $60 trillion, magnifying underlying asset risk by tens of times. Today, that doesn't exist.

This isn't the next 2008. The scale isn't enough, the leverage isn't enough, and there's no CDS nuclear-grade proliferation tool.

But several things that didn't exist in 2008 keep me from relaxing completely.

The biggest one: AI is directly impacting 40% of borrowers. When in history has a single technological force simultaneously hit such a high proportion of debtors? Never. The subprime crisis hit homeowners, not all borrowers. This time is different.

Then there's retailization. In 2008, MBS investors were primarily institutions; institutions react slowly but predictably under stress. In 2026, private credit is rapidly opening to retail investors — OBDC II is a living example. Retail panic thresholds are much lower than institutional ones, and social media has compressed the unit of confidence collapse from "months" to "hours." FSK's 15.2% drop on earnings day wasn't a market correction — it was a stampede.

And one more thing few mention: risk is being transferred. Where did the $1.4 billion in loans Blue Owl sold go? Insurance companies and pension funds. European insurance companies' private credit exposure has reached €514 billion; U.S. public pension fund allocations rose from 2.9% in 2020 to 4% in 2024. Risk hasn't disappeared — it's been transferred from where you can see it to where you can't.

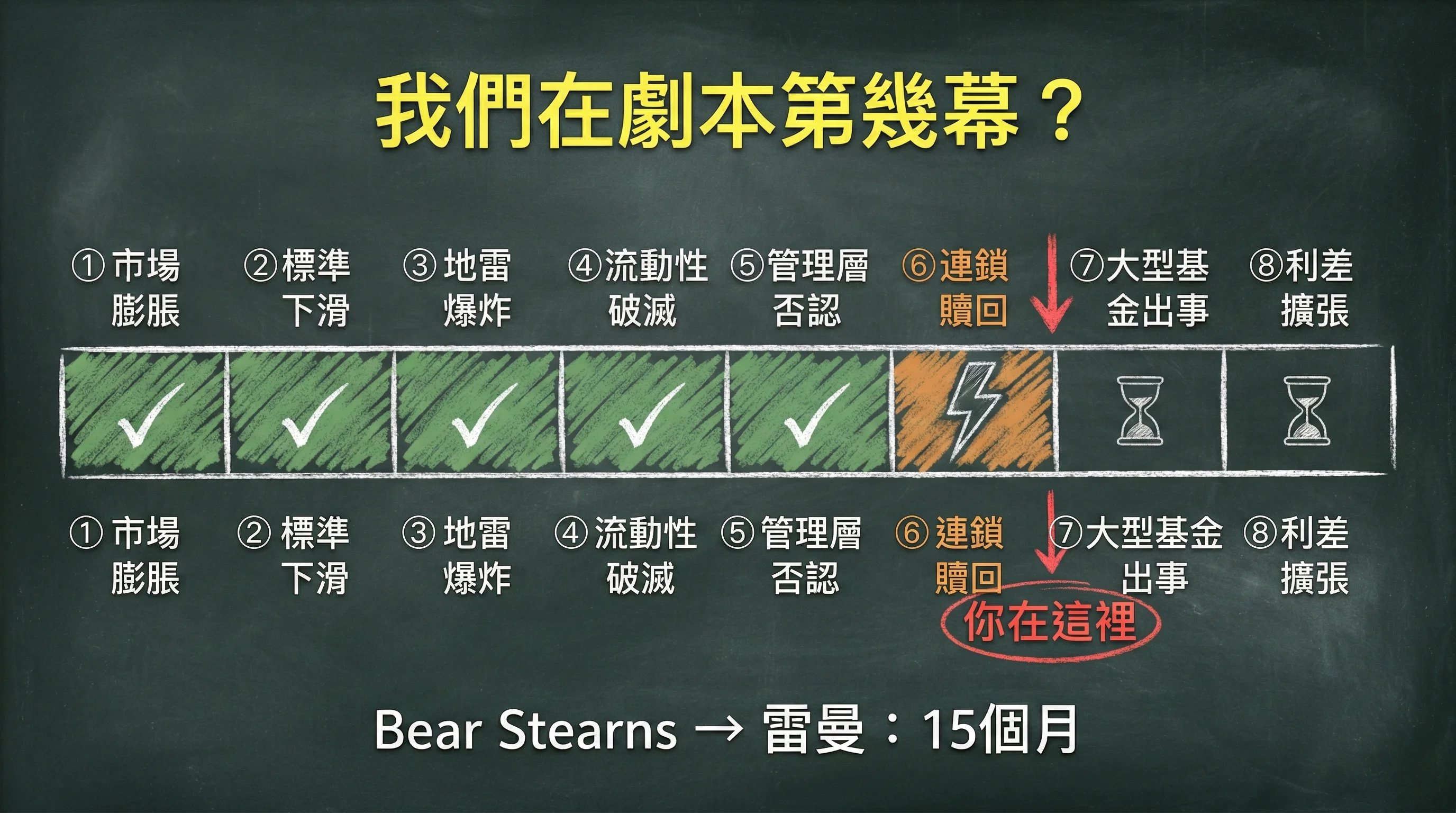

The Progress Bar: What Act Are We In?

Every credit cycle follows the same playbook. I didn't invent this — it's a behavioral sequence that checks out in every post-mortem of every cycle.

✅ Rapid market growth ($300B to $1.8T). Done.

✅ Lending standards decline (Covenant-lite, PIK become standard). Done.

✅ First mines detonate (Tricolor, FirstBrands bankruptcy). Done.

✅ Liquidity illusion shatters (Blue Owl permanently cancels redemptions, FSK drops 15.2% in a day). Done. This act moved faster than I expected — Blue Owl didn't even bother with "suspension," going straight to permanently changing the rules.

✅ Management denial ("short-term difficulty"). Done.

⚡ Chain redemptions spread to other funds. Pressure emerging. Non-traded BDC redemption wave accelerating; Blue Owl forced to dump $1.4 billion in assets. Still isolated events for now, but Bear Stearns fund suspension of redemptions in 2007 was also treated as an isolated case.

⏳ Major BDC or fund blows up. Watch. 2026 has $12.7 billion in BDC debt maturing — a 73% increase from 2025. The maturity wall hitting refinancing difficulties is the most likely combination to detonate the next act.

⏳ Credit spreads blow out significantly. Watch.

Using Bear Stearns fund suspension (June 2007) as an anchor, Blue Owl's permanent redemption cancellation (February 2026) is at a similar position — arguably even more aggressive. Bear Stearns only suspended; Blue Owl rewrote the rules. From Bear Stearns to Lehman's bankruptcy: 15 months.

Five acts completed, one in progress. That doesn't mean something will definitely happen in 15 months, but you need a set of signal lights to track.

Your Action Checklist

You don't need to panic. Panic is the worst investment strategy. What you need is to know.

Check your retirement accounts. Log into your 401k, search for "private credit," "direct lending," "BDC," "alternative." If there are results, note the percentage of your total allocation. This isn't about selling today — it's about knowing where you're exposed. Check your insurance products. Most people haven't looked at where their annuity and universal life premiums are invested since the day they bought the policy. Call your insurance company and demand to see the investment breakdown. Those $1.4 billion in loans Blue Owl sold? The buyers were insurance companies and pension funds. The premiums you pay may be holding these loans right now. Get to know the BDC sector. FSK, ARCC, MAIN, OBDC. Many people bought them for the 7-10% yield. Now you need to track one thing: NAV discount levels. Individual BDC volatility is stock-specific risk; when the entire BDC sector weakens together, that's the signal that credit risk is spreading. Understand the Fed's catch-22. Private credit uses floating rates, typically SOFR plus 500 basis points. A 25 basis-point Fed cut saves a company with $100 million in debt $250,000 a year — for a software company whose revenue is being eroded by AI, that's basically zero. What would actually make a difference is cutting 200-300 basis points, but that means the economy is already in recession. And if the economy is in recession, the borrowers' problem isn't whether rates are too high — it's whether revenue still exists. Don't cut: interest kills you. Cut big: the economy is already rotting. It's a no-win trap. The SEC passed new BDC liquidity stress test rules at the end of 2025, but implementation isn't until 2027 — too far away to save what's near. Track the progress bar. Save this, check weekly:🟢 BDC sector: Individual stock volatility is normal. Sector-wide weakness should raise alarms. Multiple suspensions of redemptions is a red light.

🟢 Default rates: 5-6% is the current baseline. Rising to 8-10% means reduce exposure. Breaking 12% — run.

🟢 Credit spreads: Modest widening isn't concerning. Expansion of 200+ basis points warrants attention. 500+ basis points is 2008 territory.

🟢 Management commentary: Those who openly acknowledge pressure are actually more credible. Beware those who say "short-term difficulty." Most dangerous are those who say "liquidity is ample" — historically, every time someone has said this, liquidity dried up within six months.

Buffett once said: "Only when the tide goes out do you discover who's been swimming naked."

The tide hasn't fully receded. But it's receding. You don't need to make any trades today. What you need today is to figure out one thing: where is your money, and what exactly are you holding?

Know what you own.

_(Data sources: Robinhood Investor's Guild, IMF, Moody's, WithIntelligence, Blue Owl Capital public statements, FS KKR financials, BLS CPI historical data. Corrections welcome if any data errors are found.)_

_—Kinney's Wonderland_